lcva2

Introduction

Again in November 2023, I wrote my first article on multinational enterprise providers supplier Teleperformance SE (OTCPK:TLPFF, OTCPK:TLPFY). On the time, TP shares have been buying and selling at round €140, nicely beneath their all-time excessive of €400 in 2021. What seemed like a deep worth alternative at first look, nonetheless, turned out to be not that low-cost in spite of everything contemplating the challenges of the enterprise.

5 months later, TP inventory worth has fallen to lower than €90, nearly 40% beneath the extent on the time of publication of my first article. So on this replace, I clarify why I consider the share worth now affords ample margin of security to justify a powerful purchase. As I detailed Teleperformance’s fundamentals again in November, I will not repeat every part on this replace, however I’ll after all check out the 2023 full-year outcomes and the year-end stability sheet (the presentation and annual report will be found here).

Why TP Inventory Is A Robust Purchase Now After The Full-12 months Outcomes And One other 40% Value Decline

Fast Evaluation Of Teleperformance’s 2023 Outcomes

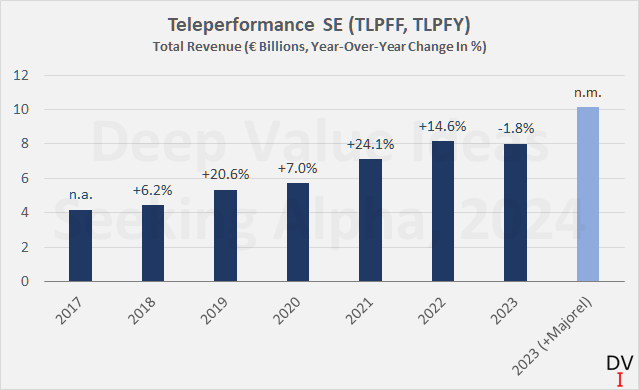

For 2023, administration reported income development of simply 2.3% in comparison with the earlier 12 months, a big decline in comparison with earlier years. Excluding the contribution from Majorel (the acquisition was announced in April 2023 however is simply consolidated since November 1, 2023), income even fell by 1.8% year-over-year on a comparable foundation (Determine 1).

Nevertheless, Teleperformance benefited considerably from the pandemic and secondary results, so the efficiency in 2021 and 2022 must be interpreted as front-loaded development. With this in thoughts, I take into account TP’s normalized longer-term development to be very stable certainly – a CAGR of 11.4% since 2017. Majorel might be a big contributor to gross sales going ahead, and hypothetically assuming it was consolidated initially of 2023, TP would have generated income of round €10 billion (mild blue bar in Determine 1).

Determine 1: Teleperformance SE (TLPFF, TLPFY): Complete income since 2017, 2023 knowledge together with and excluding the impression from the Majorel acquisition (personal work, primarily based on firm filings)

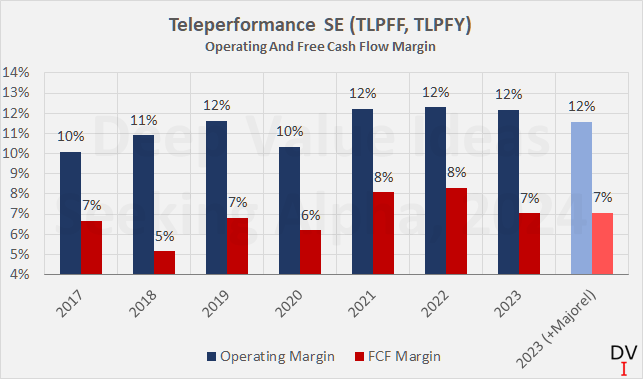

Issues additionally look good when it comes to profitability (Determine 2), however be aware the comparatively weak free money circulate (FCF) conversion. Whereas the speed has improved considerably in recent times, a money conversion price of 46% (slide 35, earnings presentation) nonetheless leaves room for enchancment.

The acquisition of Majorel will dilute Teleperformance’s profitability considerably, at the very least within the close to future. On slide 13 of the earnings presentation, administration famous that TP together with Majorel would have an adjusted EBITDA margin of 20.6%, 100 foundation factors decrease than the legacy Teleperformance. The adjusted working margin together with Majorel can be about 90 foundation factors decrease.

As an apart, please be aware that the margins proven in Determine 2 are typically primarily based on precise reported figures, excluding the impression of goodwill impairments, however together with different gadgets thought-about by administration to be “non-recurring” or “non-cash”, corresponding to stock-based compensation. SBC particularly are comparatively important at Teleperformance (8% of working money circulate most not too long ago). I’ve no situation with this in precept, however I take into account its impression to be related and subsequently deal with it as a “money expense”, because the efficiency shares granted (or choices exercised) will finally need to be repurchased to offset dilution.

Determine 2: Teleperformance SE (TLPFF, TLPFY): Working and free money circulate margin, changes defined within the textual content and within the earlier article (personal work, primarily based on firm filings and personal estimates)

Going ahead, margin growth is anticipated as Majorel is built-in, implementation prices are eradicated and synergies are realized. By 2025, administration expects to spend €100 million on the combination of Majorel and thereby notice annual – recurring – synergies of €150 million, of which €50 million are anticipated to be realized in 2024. Because of this, the working and free money circulate margin ought to enhance within the coming years. Nevertheless, there’s a important integration threat – as I defined intimately in my earlier article – so I personally take a extra conservative strategy in my up to date valuation beneath and don’t account for merger-related synergies.

That mentioned, I do not wish to be misunderstood as being skeptical in regards to the Majorel acquisition. I believe it is a wonderful match and Teleperformance has clearly demonstrated its capacity to develop inorganically as nicely. On this context, I believe it’s optimistic that Bertelsmann in addition to Saham Buyer Relationship Investments and Saham Outsourcing Luxembourg (they beforehand managed 39.4% of Majorel’s share capital) have agreed to obtain a part of the consideration within the type of Teleperformance shares. Because of this, the Saham Group and the Bertelsmann Group now every maintain 3.6% of Teleperformance’s share capital.

A Recent Look At The Stability Sheet Of Teleperformance

Earlier than continuing with the valuation, let’s take a recent take a look at Teleperformance’s stability sheet. As I defined in my final article, the acquisition was financed not solely by issuing new shares (the variety of TP shares excellent elevated by round 4 million to 64 million), but in addition by debt.

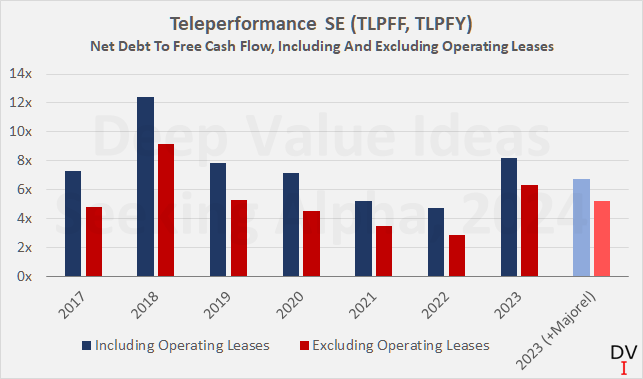

On account of the takeover, TP’s internet debt has nearly doubled in comparison with the top of 2022 – from €1.9 billion to €3.7 billion. The leverage ratio, measured by internet debt in relation to common FCF over the past three years, elevated from 2.8 to six.3 (Determine 3). Together with the estimated FCF contribution from Majorel, however excluding synergies for causes of prudence, the leverage ratio can be 5.2x FCF. If we embody working lease liabilities, the leverage ratio can be 8.2x and 6.7x with out and with Majorel’s estimated FCF contribution, respectively (Determine 3, mild blue and lightweight purple).

Determine 3: Teleperformance SE (TLPFF, TLPFY): Internet debt to free money circulate, together with and excluding working lease liabilities and the estimated free money circulate contribution from Majorel (personal work, primarily based on firm filings and personal estimates)

That is definitely a big quantity of debt, and given the up to date debt maturity profile (Determine 4), it’s clear that Teleperformance ought to prioritize debt paydown – particularly contemplating €1.3 billion of upcoming maturities in 2028 and 28% floating price debt.

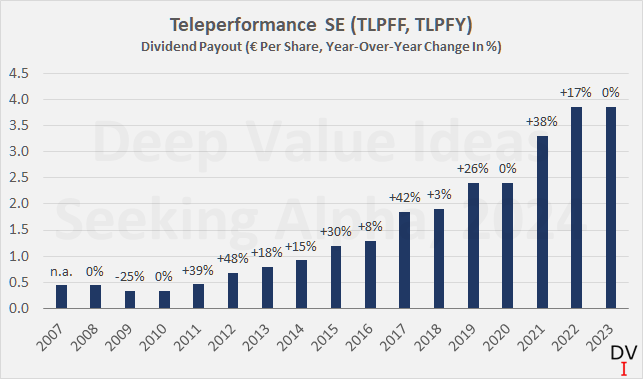

In his remarks (about 50 minutes into the conference call), CFO Olivier Rigaudy was very clear – Teleperformance “will do no matter it takes” to take care of its BBB score from S&P. Internet debt ought to fall to lower than 2x EBITDA by year-end 2024 (it was 2.56x at year-end 2023). The truth that he introduced up shareholder returns after addressing debt may be very reassuring in my view because it underlines administration’s long-term view and conservative strategy. In fact, which means the dividend may stay flat for an additional 12 months (Determine 5, present yield 4.4% however have in mind the French dividend withholding tax), and I would not fully rule out a modest dividend reduce both. Nevertheless, we also needs to not neglect that Teleperformance has dedicated to return as much as 2/3 of its FCF to shareholders through dividends and share buybacks, with the latter amounting to €366 million final 12 months. Due to this fact, I believe it’s potential that with the concentrate on deleveraging, the dividend may take priority over ongoing share buybacks.

Determine 4: Teleperformance SE (TLPFF, TLPFY): Debt maturity profile, as of December 31, 2023 (personal work, primarily based on firm filings and personal estimates) Determine 5: Teleperformance SE (TLPFF, TLPFY): Dividend per share and year-over-year dividend development (personal work, primarily based on firm filings)

Valuation Of TP Inventory – Priced For Decline

As famous within the introduction, Teleperformance shares have fallen by nearly 40% since my first article and are presently buying and selling at ranges final seen in 2016, when the corporate generated revenues of €3.6 billion and FCF of round €200 million. Teleperformance has since advanced into a way more diversified and stronger firm, greater than doubling its income and nearly tripling its FCF. Traders are presently shunning TP shares due to the narrative that synthetic intelligence may render the corporate out of date. As I defined in my first article, I consider this threat is simply partially justified, attributable to Teleperformance’s main place in its subject and the truth that the corporate began utilizing synthetic intelligence instruments years in the past. For my part, the reality is someplace within the center, however I nonetheless require a big margin of security for such an funding – additionally given the combination threat underlying the acquisition of Majorel and the excessive leverage.

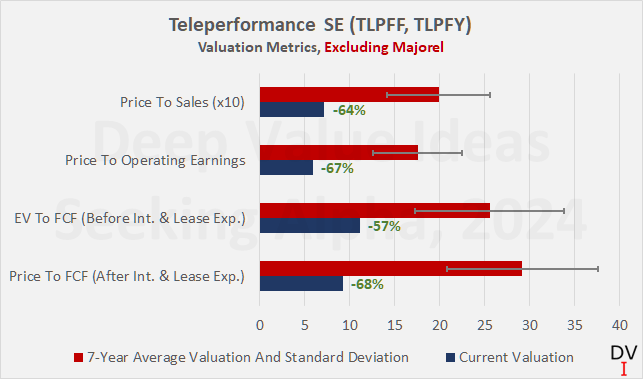

Determine 6 exhibits an up to date historic valuation of TP inventory, in response to which Teleperformance is considerably undervalued – by 60% to 70% relying on the metric, and the present valuation multiples don’t even consider the impression of Majorel, however the enterprise worth (EV) used to calculate the EV-to-FCF ratio is definitely primarily based on the 2023 year-end stability sheet, so it consists of the acquisition-related debt. I notice that that is in all probability an excessively conservative strategy to valuing the inventory, so Determine 7 exhibits a comparability of the historic common valuation to the multiples that embody Majorel’s estimated gross sales, working revenue and free money circulate contribution. TP inventory does certainly look obscenely low-cost.

Determine 6: Teleperformance SE (TLPFF, TLPFY): Historic multiples-based valuation, present valuation metrics don’t embody Majorel’s estimated income, working revenue and free money circulate contribution (personal work, primarily based on firm filings and personal estimates) Determine 7: Teleperformance SE (TLPFF, TLPFY): Historic multiples-based valuation, present valuation metrics embody Majorel’s estimated income, working revenue and free money circulate contribution (personal work, primarily based on firm filings and personal estimates)

Nevertheless, skeptical traders may argue that the historic valuation isn’t a fairly reasonable benchmark on this case. What if the times of double-digit development at Teleperformance are certainly over? What if AI finally makes Teleperformance’s enterprise mannequin out of date?

What I love to do in such instances is to give you a really conservative valuation strategy. Some time in the past, I wrote an article on the valuation of tobacco corporations wherein I assumed a fast decline in gross sales and working profitability. On the instance of the second-tier cigarette producer Imperial Manufacturers p.l.c. (OTCQX:IMBBY, OTCQX:IMBBF), I confirmed that traders can count on a stable return even when these notably adverse situations materialize.

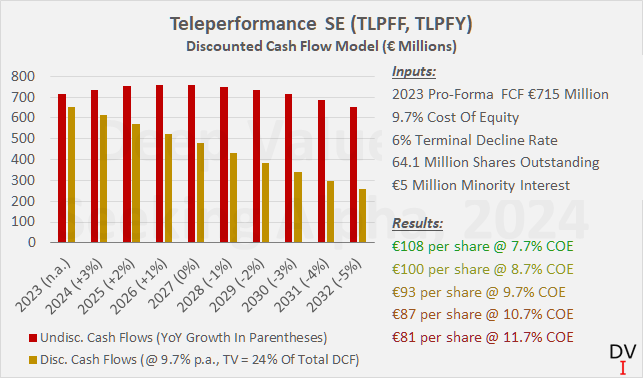

Within the case of Teleperformance, I began with free money circulate together with the anticipated contribution from Majorel, however ignoring potential value synergies. I’ve assumed an FCF development price of three% for 2024, which is in step with administration’s development steering for the 12 months. I then modeled a 100 foundation level annual decline within the development price and maintained the -6% annual decline in free money circulate beginning in 2033. Frankly, I extremely doubt this would be the way forward for Teleperformance (the truth is, I consider the corporate can at the very least keep its present free money circulate), however even when it does, TP inventory remains to be low-cost in the present day.

Assuming that an investor is comfy with a value of fairness of 9.7% (as per my earlier article), the inventory can be pretty valued at €93 underneath the belief of terminal decline. At in the present day’s share worth of €87, a value of fairness of 10.7% is subsequently a sensible return expectation. And if Teleperformance is certainly in a position to keep its present free money circulate, traders can be taking a look at 11.5% p.a. (sensitivity evaluation in Determine 9).

Determine 8: Teleperformance SE (TLPFF, TLPFY): Discounted money circulate valuation a number of – conservative strategy, terminal decline (personal work, primarily based on firm filings and personal estimates) Determine 9: Teleperformance SE (TLPFF, TLPFY): Discounted money circulate sensitivity evaluation (personal work, primarily based on firm filings and personal estimates)

All in all, there isn’t a denying that the market is extraordinarily adverse on Teleperformance shares in the intervening time. Even when one assumes that Teleperformance is an organization in decline (whereas precise development has been in double digits over the past decade!), the inventory remains to be low-cost and represents ample margin of security is enough to justify an funding.

Conclusion

As per my final article, I keep that Teleperformance is an fascinating, founder-led firm with a powerful historical past and a well-diversified enterprise. It appears to be like nicely entrenched with many main corporations and I do not assume AI must be seen as an outright headwind for the corporate, not to mention that it may finally render TP out of date. Teleperformance is a frontrunner in its subject and its development monitor document over the past decade is extraordinarily stable and attributable to sturdy natural development but in addition to acquisitions. Though I believe it’s unreasonable to count on a continuation of the double-digit development charges that traders have change into accustomed to over time, I don’t see Teleperformance as an organization in decline both.

The market clearly disagrees, valuing TP shares at a 60% to 70% low cost to the 2016 to 2023 common valuation, relying on the metric is used and whether or not or not Majorel’s income and earnings contribution is included. Teleperformance’s valuation by the lens of discounted money circulate evaluation, it’s clear that the market has priced the inventory for terminal decline. With an anticipated value of fairness of 10%, the corporate’s free money circulate may decline at an accelerating price from 2028 onwards. Even when free money circulate falls by 6% per 12 months from 2033, the inventory remains to be undervalued at its present worth of €87.

For my part, this can be a enough margin of security. I subsequently not too long ago initiated a place in TP inventory at roughly €90, representing roughly 0.3% of my portfolio and which I count on so as to add to over the approaching weeks and possibly months.

Thanks very a lot for studying my newest article. Whether or not you agree or disagree with my conclusions, I all the time welcome your opinion and suggestions within the feedback beneath. And if there’s something I ought to enhance or increase on in future articles, drop me a line as nicely. As all the time, please take into account this text solely as a primary step in your due diligence.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}