CHUNYIP WONG

Funding Thesis

Power Switch (NYSE:ET) is an power firm that focuses on transporting and storing pure gasoline and propane pipelines. It has not too long ago introduced the acquisition of Lotus Midstream which I imagine can speed up its progress as demand within the Permian basin has been constant, and it additionally supplies entry to key producers. The corporate additionally has a excessive dividend payout, making it a horny choice for risk-averse buyers to achieve a hard and fast earnings.

About ET

ET is an power agency working within the U.S. that offers within the transportation and storage of pure gasoline & propane pipeline. The corporate conducts its enterprise in eight segments: Intrastate transportation & storage, Interstate transportation & storage, Midstream, Crude oil transportation & providers, NGL & refined merchandise transportation and providers, Funding in Sunoco L.P., Funding in USAC, and All different segments. The Intrastate transportation & storage phase owns and operates pure gasoline transportation pipelines of 11,600 miles. This phase carries out the logistics of pure gasoline to main markets in numerous areas from Texas & Louisiana, the place pure gasoline is produced. This phase generates 7.20% of the corporate’s complete income. The interstate transportation phase affords a broad array of storage and pipeline providers to prospects within the Canada, Gulf Coast, Midwest, Southeast, and Southwest area via interstate pure gasoline pipelines of 19,945 miles. This phase earns 2.10% of the corporate’s complete income. Within the midstream trade, pure gasoline is gathered, compressed, handled, processed, saved, and transported. It carries out its operations in prime manufacturing basins positioned in Texas, Ohio, West Virginia, Pennsylvania, Louisiana, Arkansas, and Oklahoma. This phase represents 15.70% of the corporate’s complete income. The Crude oil transportation & providers phase affords transportation, advertising and marketing, terminalling, and acquisition providers to prospects in crude oil markets of the Midwest, southwest, and Northeastern United States. The corporate operates crude oil trunk & gathering pipelines of 11,315 miles via this phase. This phase contributes 23.90% to the corporate’s complete income.

The NGL & refined merchandise transportation and providers phase affords transportation, storage, mixing, and execution of acquisitions & advertising and marketing actions via its complementary pipeline community & storage amenities. This phase generates 23.60% of the corporate’s annual income. Sunoco L.P. distributes motor fuels to unbiased sellers, wholesalers, industrial prospects, and end-user prospects at retail areas operated by fee brokers. This phase represents 23.64% of the corporate’s complete yearly revenues. USAC affords pure gasoline compression providers in Utica, Marcellus, Permian Basin, Eagle Ford, Granite Wash, Haynesville, and Fayetteville shales. This phase contributes 0.60% to the corporate’s complete income. The ‘All-other’ phase consists of gasoline advertising and marketing actions, pure gasoline compression gear enterprise, and different subsidiaries that are concerned within the transportation of pure gasoline. This phase accounted for about 3.30% of the corporate’s complete income.

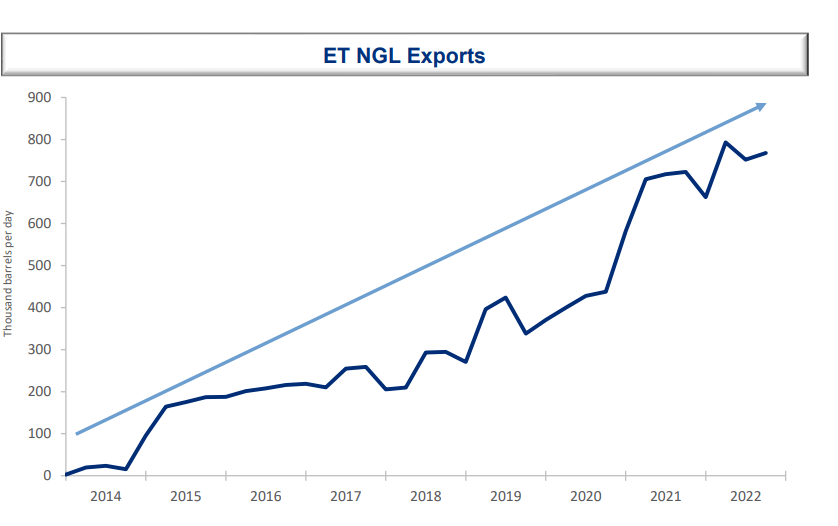

ET NGL Exports (Investor Presentation: Slide No: 17)

Acquisition of Lotus Midstream

Pure gasoline performs an important function within the clear power transition course of, which has triggered a speedy improve in its demand. Most international locations are adopting new insurance policies which have considerably accelerated the funding and exports of pure gasoline in recent times. These progress dynamics have created ample alternatives for all of the individuals within the pure gasoline trade. Figuring out these alternatives, the corporate has not too long ago introduced the acquisition of Lotus Midstream. ET acquired the Lotus Midstream for $1.45 billion. Lotus Midstream offers in proudly owning & managing crude pipeline and terminal programs positioned within the Permian Basin, which covers very important manufacturing areas with a capability of 1.5 million barrels per day. As per this acquisition deal, transportation pipeline and crude gatherings will likely be prolonged from Southeast New Mexico via the Permian basin in West Texas to Cushing, Oklahoma, masking 3000 miles. It would broaden ET’s Texas storage capability by 2 million barrels. This acquisition additionally consists of fairness curiosity within the Wink to Webster pipeline of 5% which is able to assist the corporate to move crude oil above a million barrels per day via a 650-mile pipeline system to the Gulf Coast. I imagine this acquisition can act as a major catalyst to speed up the corporate’s progress as it could assist it to boost its presence within the Permian basin, the place the demand has been constant. I feel this acquisition may also help ET. to spice up its transportation & storage enterprise and scale back the chance of inconsistent provide to a big extent, as Lotus Midstream may also help it to achieve important volumes from the important thing producers and improve its connectivity to the market. Because the pipelines will lengthen, the corporate can anticipate a rise in fee-based revenues, and the money move is estimated to extend regularly, which alerts the expansion of quarterly dividends. As per my evaluation, this acquisition also can assist ET to seize further market share and broaden its revenue margins, because the Centurion pipeline system of Lotus Midstream can improve the publicity of ET to the most important hubs of Midland, Wink, and Crane. I feel the corporate can additional maintain this progress and anticipate further income progress within the subsequent yr as ET can be planning to construct a 30-mile pipeline venture which is able to assist it in originating barrels from Midland terminals to Cushing.

Monetary Tendencies

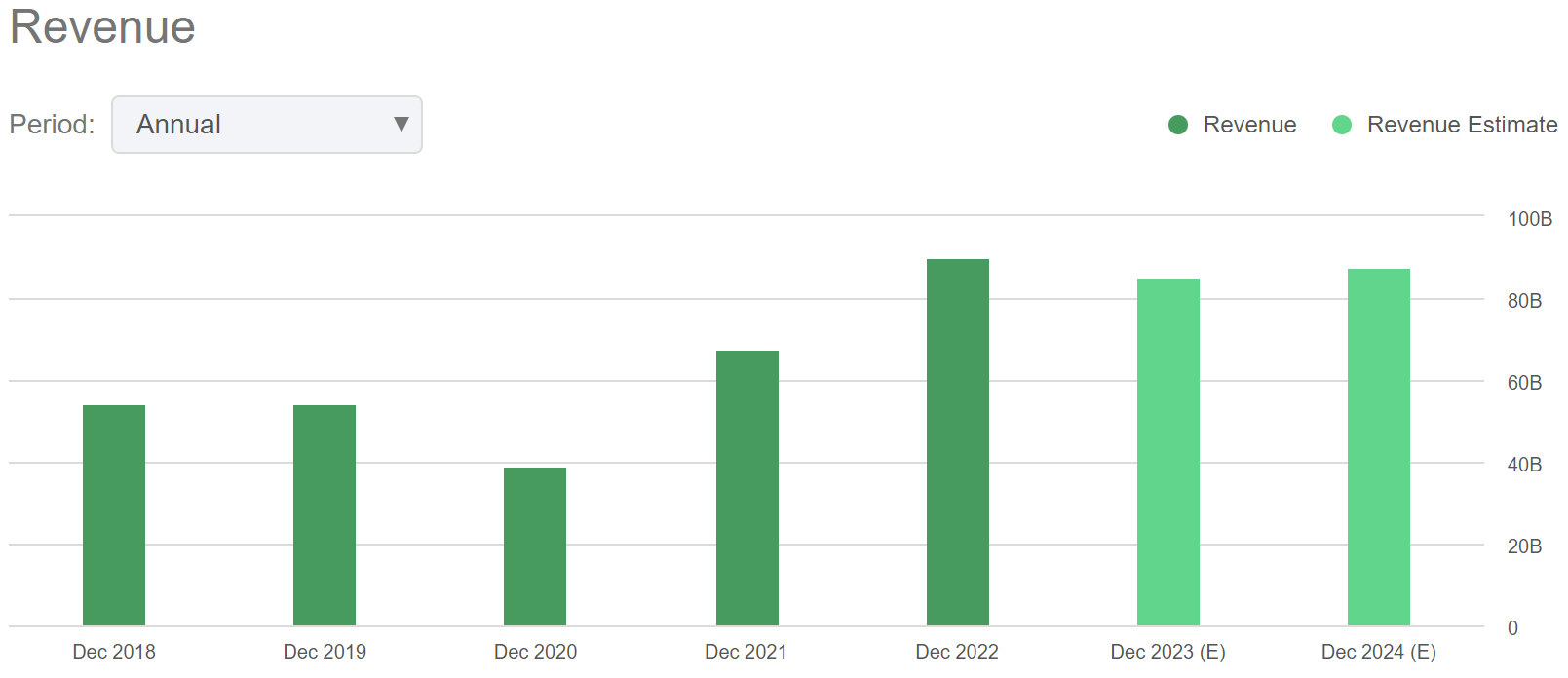

Income Pattern of ET (Searching for Alpha)

The income has grown from $54.09 billion in FY2018 to $89.88 billion in FY2022, leading to a strong 5-year CAGR of 10.7%. The corporate has skilled a major lower in income in FY2020 resulting from uncertainty out there attributable to the pandemic. The corporate reported a income of $89.88 billion in FY2022, a progress of 33.31% in comparison with $67.42 billion in FY2021. In response to Searching for Alpha, the corporate would possibly expertise a slight lower in income in coming years, however it is rather excessive in comparison with the pre-pandemic ranges. I imagine the corporate can maintain this excessive degree of income within the coming years as the corporate is experiencing robust world demand for liquefied pure gasoline (LNG) & pure gasoline liquids (NGL) and in keeping with a latest incomes name of ET, U.S. pure gasoline producers have expressed a rising curiosity in committing a share of their output to long-term gross sales contracts at LNG index pricing. In response to Searching for Alpha, the corporate’s income may be $85.39 billion and $87.49 billion in FY2023 and FY2024, respectively. I imagine these estimates completely seize the influence of the rising world demand and the acquisition of Lotus Midstream.

Excessive Dividend Yield

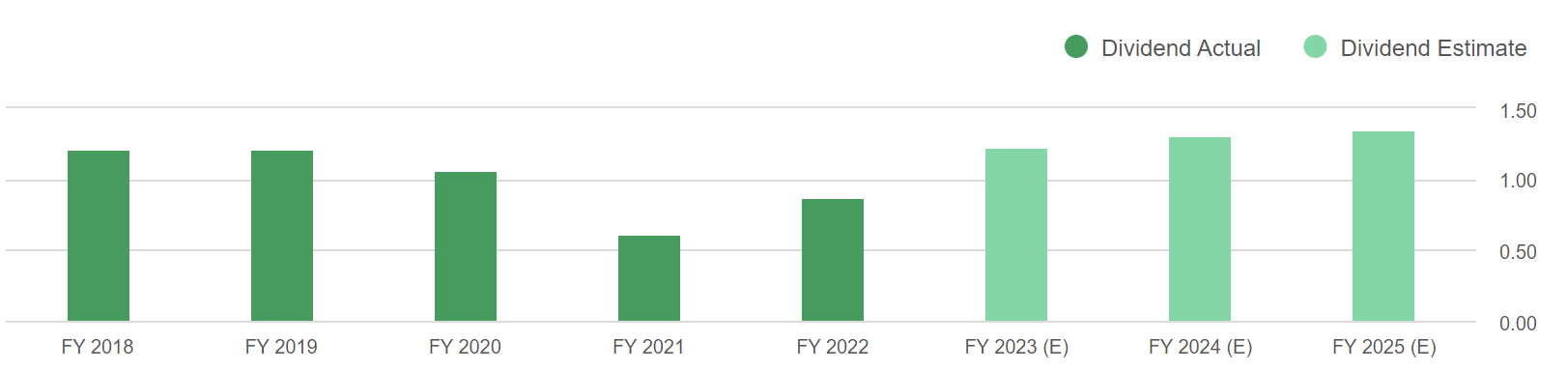

Dividend Cost Historical past (Searching for Alpha)

The corporate has a wholesome and spectacular historical past of dividend payouts from the previous a few years. Within the earlier yr, ET distributed money dividends of $0.175, $0.20, $0.23, and $0.26 in every of the 4 quarters, respectively, which makes the annual dividend $0.87, representing a dividend yield of 6.87%. After the pandemic, the corporate considerably decreased the dividend cost because of the uncertainty out there. Within the first quarter of the present yr, it distributed a money dividend of $0.305, indicating that the corporate is planning to reinstate its pre-pandemic dividend coverage.

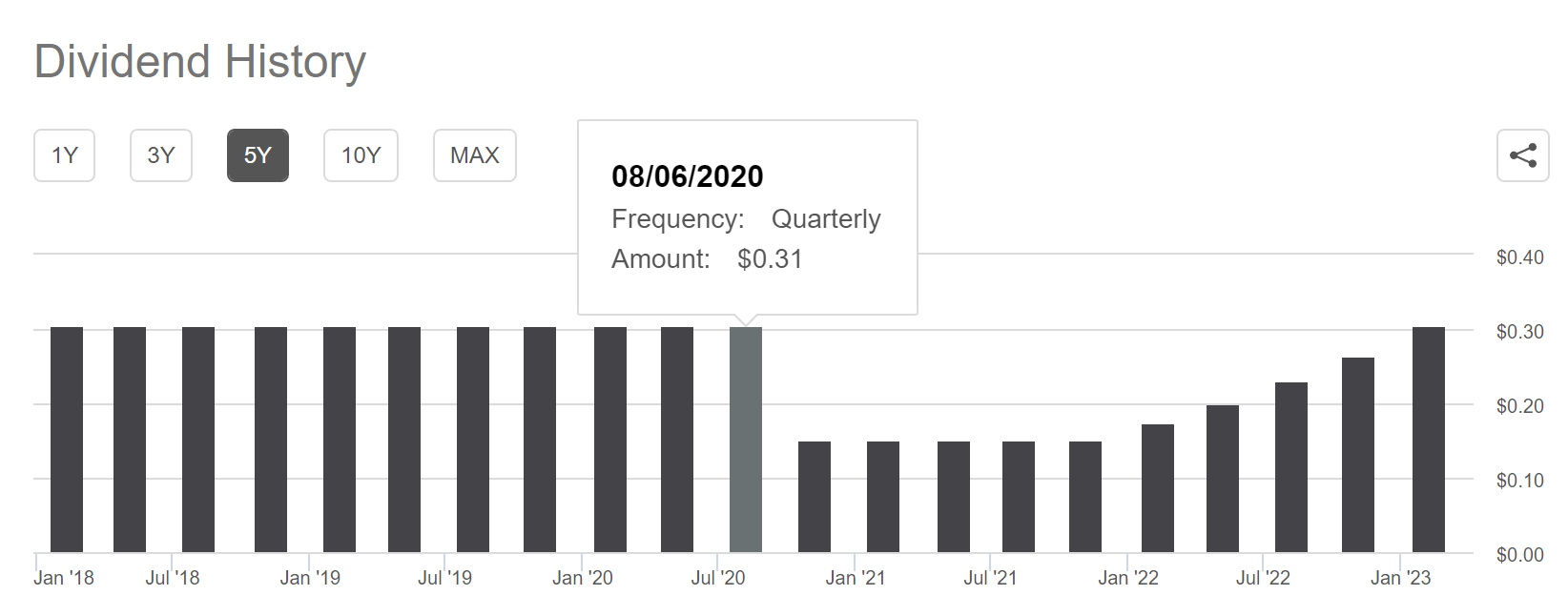

Quarterly Dividend Cost (Searching for Alpha)

I imagine the corporate can maintain this dividend payout within the coming quarters because it has not too long ago acquired Lotus Midstream, which is able to regularly improve its money move. After contemplating all these elements, I estimate that the money dividend of $0.305 can stay fixed within the subsequent three quarters, which makes the annual dividend $1.22, representing a excessive dividend yield of 9.75% in comparison with the present share worth.

What are the Dangers Confronted by ET?

Excessive dependency on key producers and worth volatility

The corporate is extremely depending on a number of the key producers for the availability of pure gasoline. The manufacturing of pure gasoline might be affected by numerous elements, resembling pure disasters, geopolitical conflicts, and different financial circumstances. If the availability of pure gasoline is interrupted or a discount in volumes of pure gasoline can extremely influence the corporate’s enterprise. A decreased provide of pure gasoline may end up in fewer transportation volumes which can additional result in a contraction within the firm’s revenue margins. As well as, pure gasoline costs are extremely unstable resulting from fluctuations in demand that are triggered resulting from inflation, provide chain disruptions, and availability of fuels. In such occasions, earnings from storage might be affected and might put stress on the corporate’s revenue margins.

Excessive Debt

The corporate has substantial long-term debt on its stability sheet. Presently, the corporate has long-term debt of $48.3 billion. The rising rates of interest can improve the corporate’s monetary value. The federal reserves are constantly rising the rates of interest to regulate inflation. If the federal financial institution decides to extend the rates of interest within the coming years, it could adversely have an effect on the corporate’s revenue margin.

Valuation

The corporate has not too long ago acquired Lotus Midstream which might considerably speed up its progress by strengthening its place within the Permian Basin, the place the demand dynamics are constructive. I imagine this acquisition can have a constructive influence on the corporate’s monetary efficiency within the coming instances as operations are being expanded to a big extent. The corporate can be experiencing robust world demand for LNG & NGL. In response to Searching for Alpha, the corporate’s EPS for FY2023 may be $1.56. After contemplating all of the above elements, I feel the Searching for Alpha’s estimates are correct. The estimated EPS of $1.56 offers the ahead P/E ratio of 8.01x. After evaluating the ahead P/E ratio of 8.01x with ET’s 5-year common P/E of 8.45x, I feel the corporate is completely valued on the present worth of $12.51.

Conclusion

Power Switch has enormous progress alternatives fueled by the quickly rising demand for LNG & NGL. The newest acquisition of Lotus Midstream may also help the corporate to keep up its progress price and assist enhance revenue margins sooner or later. As well as, I imagine this acquisition can gasoline its dividend progress within the coming years. It faces the chance of provide disruptions and pure gasoline worth volatility, which might have an effect on its monetary efficiency. Power Switch additionally has enormous debt on its stability sheet. In response to my evaluation, the corporate is completely valued on the present share worth. Nonetheless, the corporate is reinstating its pre-pandemic dividend coverage. I imagine the buyers can maintain of their portfolio to earn a strong dividend yield of 9.75%. After analyzing all of the above elements, I assign a maintain score for ET.

{kind=link}