VanderWolf-Photographs/iStock Editorial through Getty Photographs

Firm description

Wizz Air Holdings Plc (OTCPK:WZZAF / OTCPK:WZZZY) gives passenger air transportation companies on scheduled short-haul and medium-haul point-to-point routes in Europe and the Center East. Their fleet of 154 plane operates companies for round 1000 routes from 194 airports in 51 international locations.

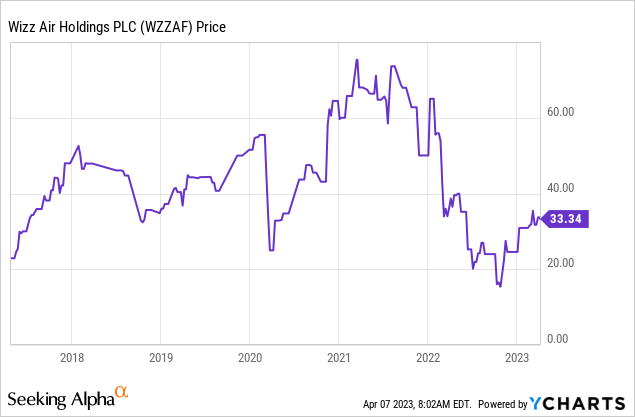

Share value

Wizz’s share value was trending up earlier than the pandemic however now appears to be much more unstable. Good points had been made in late 2020 because the prospect of returning journey loomed however this shortly reversed as the truth of a number of lockdowns and smooth air journey grew to become obvious. Wizz is now buying and selling solely barely increased than its 2017 value, which may symbolize a chance for buyers.

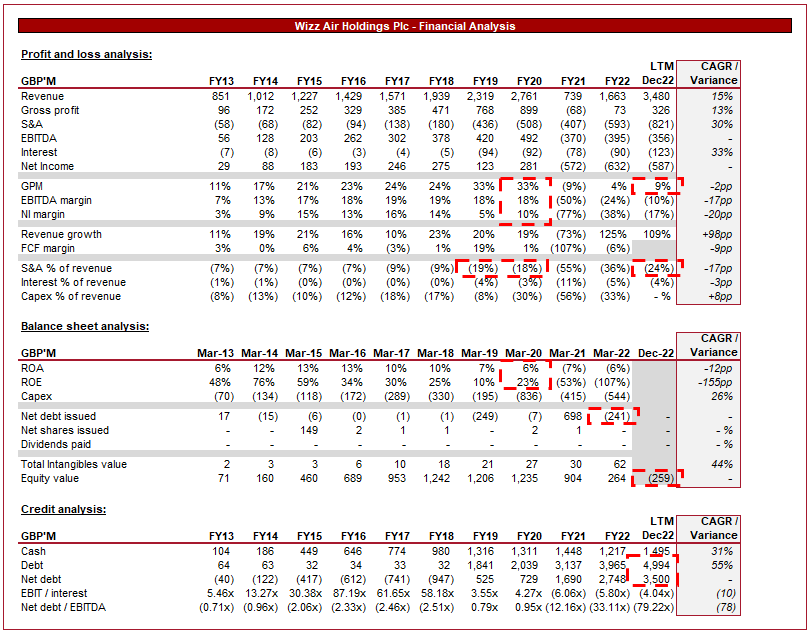

Monetary evaluation

Wizz Air Financials (Tikr Terminal)

Introduced above is Wizz’s monetary efficiency for the final decade.

Income

Regardless of the affect of the pandemic, income has grown at a powerful CAGR of 15%.

Wizz has been increasing its routes all through the last decade, doing so impressively resulting from its pricing construction. Wizz is a “loss-cost airline”, basically an airline that limits its companies and high quality as a way of driving down costs. Shoppers are high quality with this as it’s focused at those that need comfort and/or reasonably priced flights as a precedence. Low-cost carriers have been quickly gaining recognition in Europe as a larger variety of customers see much less worth within the companies that include a flight, preferring to be cost-effective as a substitute. This has allowed Wizz to realize market share from the likes of IAG.

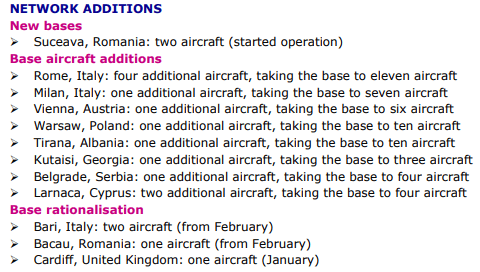

Wizz community growth (Wizz Air)

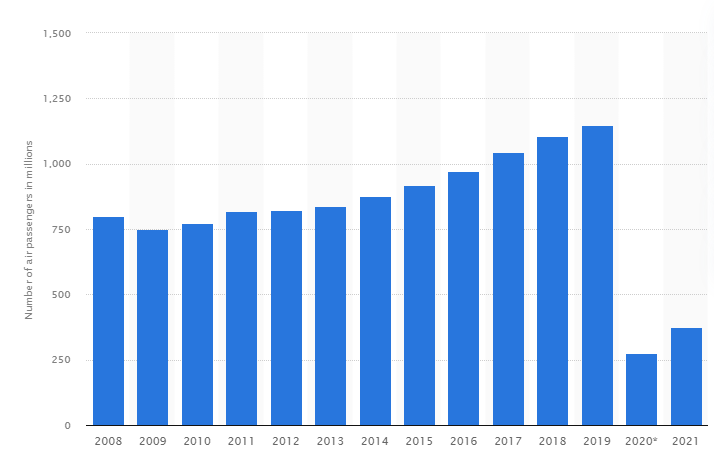

With the financial progress in Europe and rising disposable earnings, the demand for air journey has been rising steadily. As the next graph illustrates, Europe has seen a constant rise in journey numbers. Our view is that progress ought to proceed on this vein within the coming years because the affect of Covid-19 subsides.

Variety of passengers (Statista)

Wizz is repeatedly including new plane to its fleet to help its route growth plans. That is the biggest driver of income progress and has been supported by the factors acknowledged above. Wizz presently has 177 aircrafts, with a mean age of 4.6 years. This provides the corporate one of many youngest fleets in Europe, giving the enterprise a protracted runway to monetize these planes. Wizz Air has a monster supply backlog, with a complete of 388 aircrafts due for supply as of Dec22. This could enable income to develop quickly within the coming yr from quantity progress.

Wizz has additionally been capable of develop via energetic pricing. Though the enterprise is a low-cost service, it doesn’t imply Wizz can not value aggressively the place attainable. In the newest interval, Wizz has seen its Income per Accessible Seat-Kilometer (RASK) enhance as energetic pricing has not deterred folks from touring following the Covid lockdowns. load issue % has elevated to 87%, supporting the necessity for a larger variety of planes.

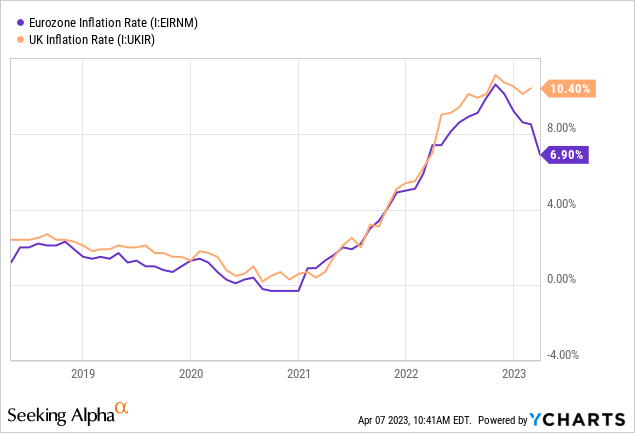

The corporate is dealing with short-term headwinds, nonetheless. We’re presently experiencing inflationary circumstances, with the Eurozone and UK inflation charges at 6.9% and 10.4% presently.

That is contributing to a decline in discretionary spending as customers see their residing prices enhance and their conduct turns defensive. Vacation spending is mostly thought of a luxurious and one thing which may be simply deferred, which many will probably do within the coming 12 months. On account of this, Wizz may see a gradual interval within the coming yr as the main target stays on bringing inflation underneath management.

One other difficulty the enterprise faces within the coming years is a change in shopper habits. The pandemic has proven that in lots of circumstances, enterprise journey is pointless and may be changed by video calls. This has contributed to a decline in enterprise journey which can not essentially bounce again as quickly as discretionary journey. Additional, progress on this phase might now gradual to a stage under the pre-Covid interval.

Margins

Wizz produced fairly implausible margins traditionally, attaining an EBITDA-M of 18% and a NI margin of 10% within the yr earlier than the pandemic. For any mature business, this can be a respectable efficiency and Wizz confirmed the power to take care of this for a number of years. The goal is to return to this stage.

At the moment, nonetheless, Wizz is critically battling margins. Regardless of income exceeding the pre-Covid ranges, every little thing under GP has not. This has been pushed largely to gasoline prices. Vitality costs are one of many predominant causes we’re seeing the degrees of inflation we’ve. As the next graph illustrates, Jet gasoline stays noticeably above the degrees we’ve seen within the final decade, making it extraordinarily tough for airliners to function at a worthwhile stage.

Jet gasoline value (S&P international)

Oil costs usually are trending down, nonetheless, it’s tough to forecast the place they’ll normalize within the coming yr. In the newest interval, Wizz has seen a 62% enhance in gasoline unit prices, reflecting the issue presently. Administration has presently hedged 59% of their deliberate consumption for FY23 and 45% for FY24.

Outdoors of gasoline prices, Administration has sought to cut back different working prices as a way of discovering efficiencies however the enterprise has struggled. S&A bills presently symbolize 24% of income, which is way increased than the FY19/20 ranges.

Primarily based on what we’re seeing with prices, it appears tough for Wizz to return to its pre-Covid profitability ranges, a minimum of within the subsequent 12-18 months.

Stability sheet

As soon as once more, Wizz’s pre-Covid ranges look extremely engaging, having constantly achieved a ROE of >20%. We frequently spotlight the pre-Covid ranges because the enterprise can return to those ranges, a minimum of as soon as macro circumstances soften.

Traditionally Wizz operated conservatively, with little debt past plane financing. This has modified on account of the pandemic, with its internet debt reaching £3,500M. At FY20’s EBITDA, this represents an ND/EBITDA ratio of 7x. The excellent news for Wizz is that it’s money circulation generative and has £1,495M, which ought to imply no quick solvency danger. This being mentioned the enterprise has a protracted highway forward to adequately deleverage its stability sheet.

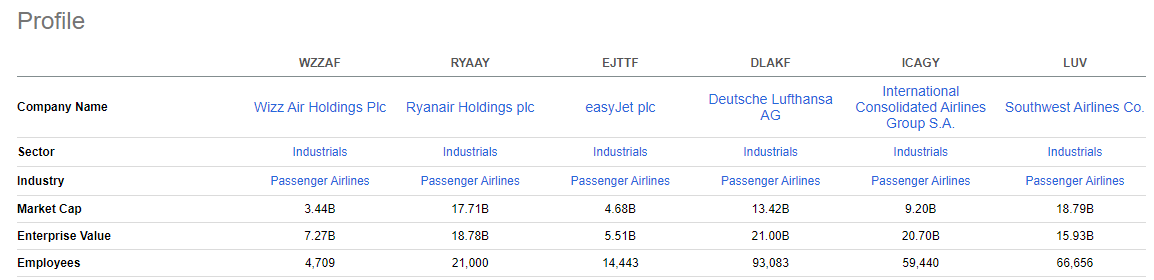

Peer comparability

Friends (In search of Alpha)

To evaluate Wizz’s relative efficiency, we’ve in contrast the enterprise to the next corporations. Nearly all of these chosen are European operators, to finest align economics.

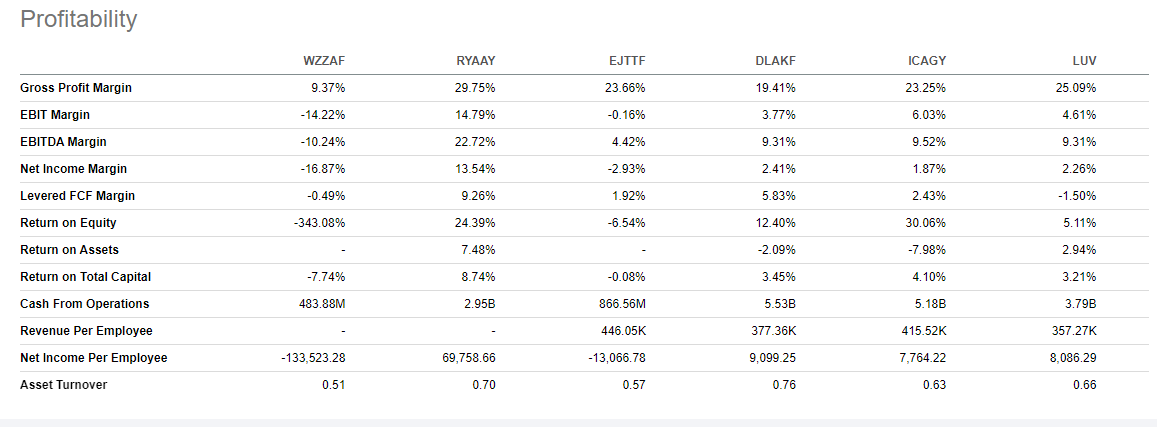

Profitability (In search of Alpha)

Wizz is an outlier based mostly on profitability, as it’s the solely enterprise that is still loss-making within the LTM interval. This can be a poor efficiency which can drag on the enterprise within the coming yr.

Progress (In search of Alpha)

Wizz scores much better from a progress perspective, suggesting that is Administration’s focus as a way of driving alpha within the medium time period. This isn’t a nasty technique because the enterprise is quickly increasing its fleet. Gaining market share throughout unsure instances earlier than transitioning again to profitability might be a method that yields good points.

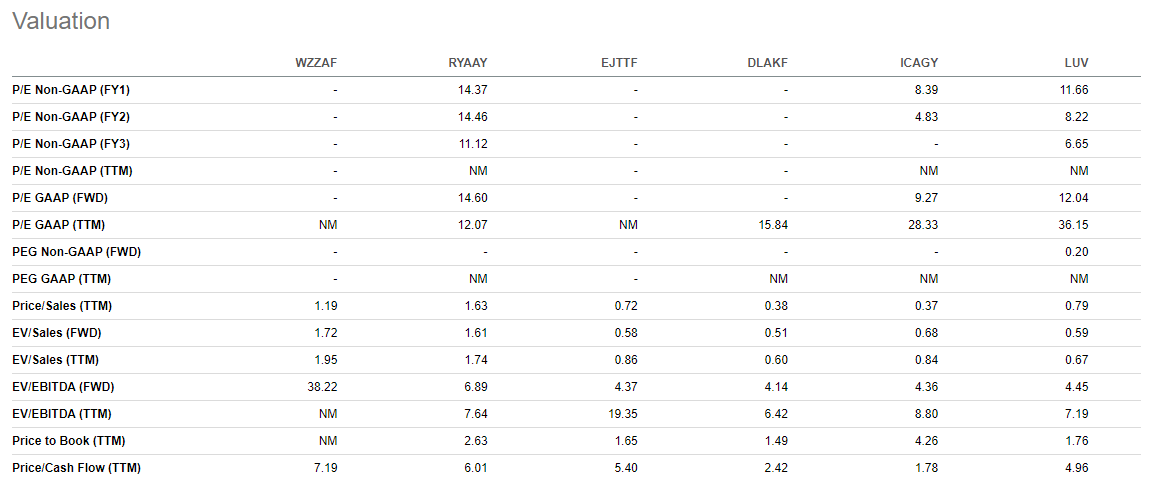

Valuation

Valuation (In search of Alpha Valuation)

Regardless of the underperformance, Wizz is buying and selling at a premium to its friends. On account of its destructive EBITDA, one of the best metric to think about is NTM EV/Gross sales. The explanation for that is probably buyers pricing in aggressive progress within the coming years, as Wizz’s order guide is step by step delivered. The important thing to Wizz’s fortunes is the place margins will normalize within the coming years.

Closing ideas

We’re an enormous fan of how Wizz has achieved progress, with it being reasonable that issues will proceed because of the backlog of planes that shall be delivered. The difficulty with the enterprise presently is that it’s tough to take a view of the place margins will land. They may definitely enhance with friends replicate as a lot. If Wizz was capable of return to its pre-Covid ranges, we might think about the enterprise extremely engaging, regardless of its excessive stage of debt. With its present premium valuation, we don’t see scope for buyers to be rewarded for taking this danger.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}