phive2015

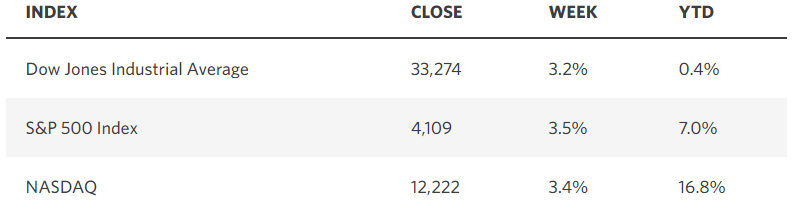

The foremost market indexes completed their finest weekly efficiency for the yr to shut out the primary quarter, which makes for back-to-back quarterly positive factors. The exclamation level was a better-than-expected inflation report on Friday, rising the probability that short-term rates of interest have peaked for this cycle. That has helped gas a rebound in development shares, led by the know-how sector, as financials and extra value-oriented names have lagged. But I count on breadth to begin bettering once more as we transfer by way of April, main the S&P 500 to shut in on a bull market achieve of 20% or extra from its October bear market low.

Edward Jones

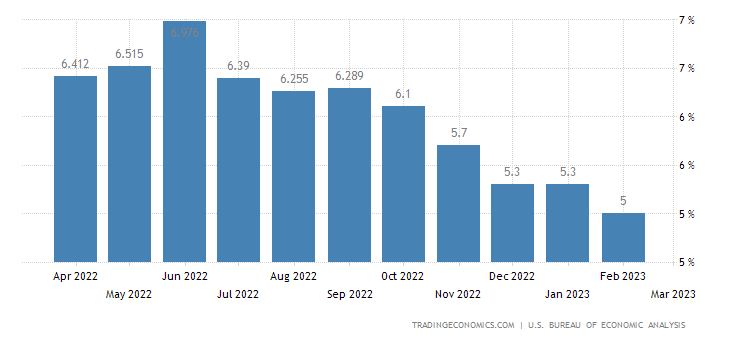

Each month the inflation hawks hold warning us about value will increase, however each month the annualized charges of inflation retains falling. On Friday, we realized that the private consumption expenditures (PCE) value index increased simply 0.3% in February, which was lower than anticipated and half the 0.6% improve in January. The core fee that excludes meals and vitality additionally rose 0.3%, which was down from a downwardly revised 0.5% in January. The year-over-year fee fell to five%, whereas the core ticked right down to 4.6%. The disinflationary development that started final June is firmly entrenched. We should always fall to a variety of 2-3% by yr finish, which might be ample to appreciate a gentle touchdown.

TradingEconomics

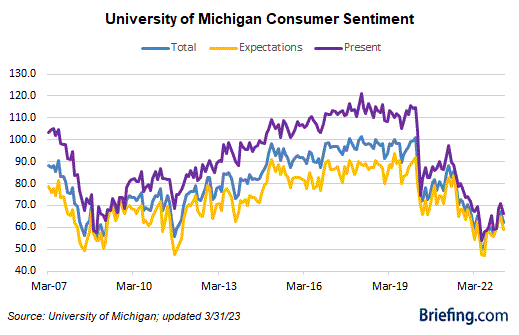

Client sentiment stays at depressed ranges, which I discover to be encouraging from a contrarian viewpoint. I feel the fixed warnings a few recession by pundits have shoppers on edge, however that has not translated right into a regarding slowdown in financial development, as actual spending development sustains itself. The excellent news out of this report is that inflation expectations for the yr forward declined once more in March to three.6% from what was 4.1% in February. That has to please Fed officers, even when they will not brazenly admit it.

Briefing.com

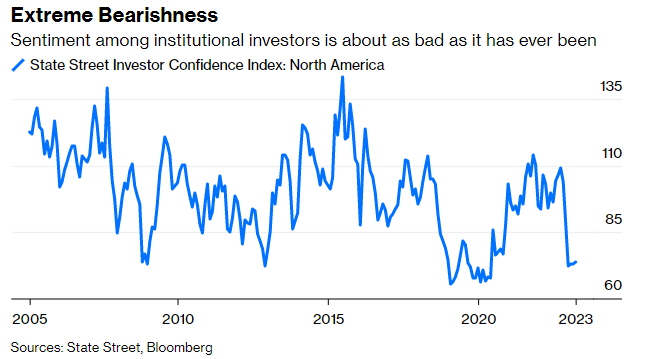

Institutional traders are simply as bitter, as measured by the precise trades they place, which is tracked by an index managed by State Road. It has but to get well from traditionally low ranges it reached late final yr. Once more, I view this as a optimistic from a contrarian standpoint.

Bloomberg

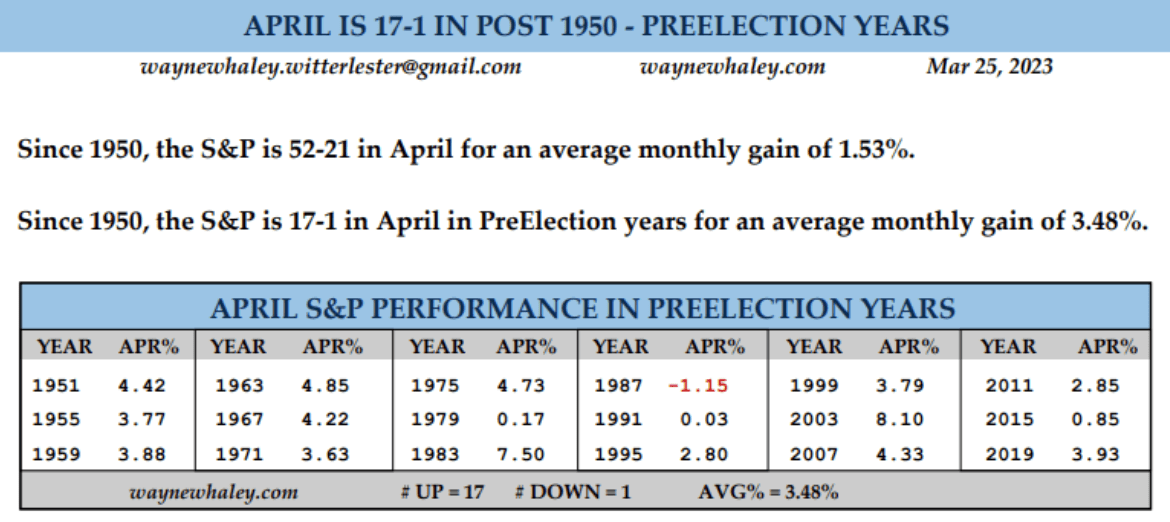

I need to end with a overview of a number of the bullish developments which have occurred because the starting of the yr main as much as April, which has traditionally been a really robust month for shares in pre-election years. The S&P 500 has risen in 17 out of the final 18 Aprils relationship again to 1950 for a median achieve of three.48%.

WayneWhaley.com

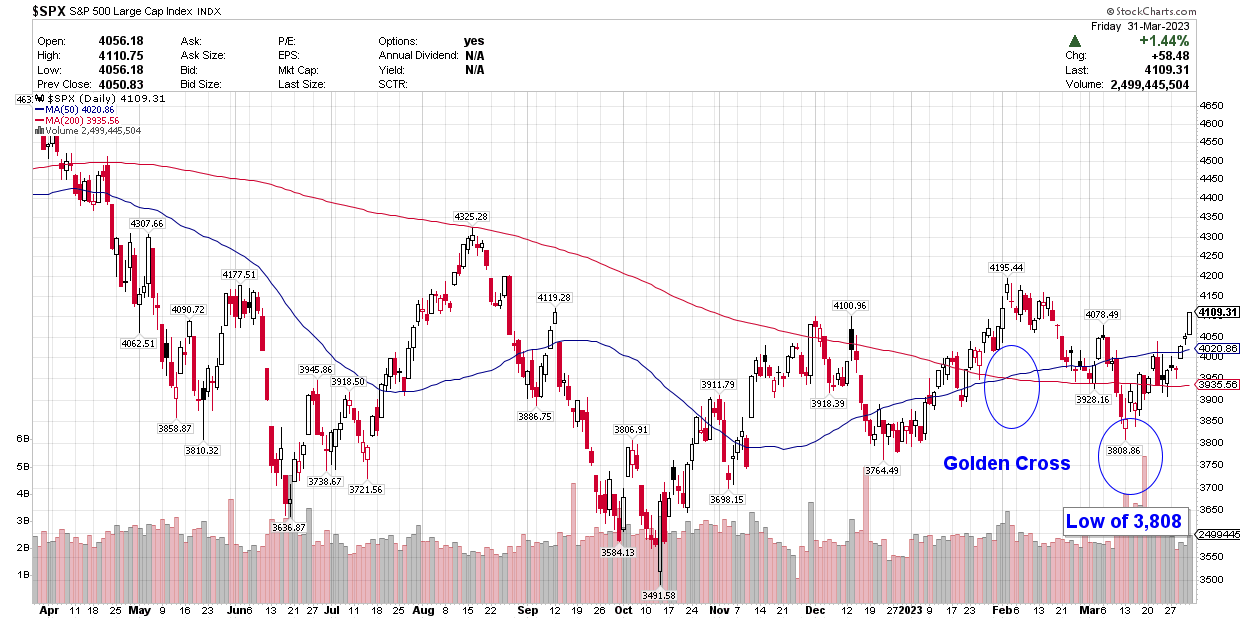

I feel the chance for positive factors this April improved after the Golden Cross that occurred for the S&P 500 in early February, which is when the 50-day shifting common crossed above the 200-day shifting common.

Stockcharts.com

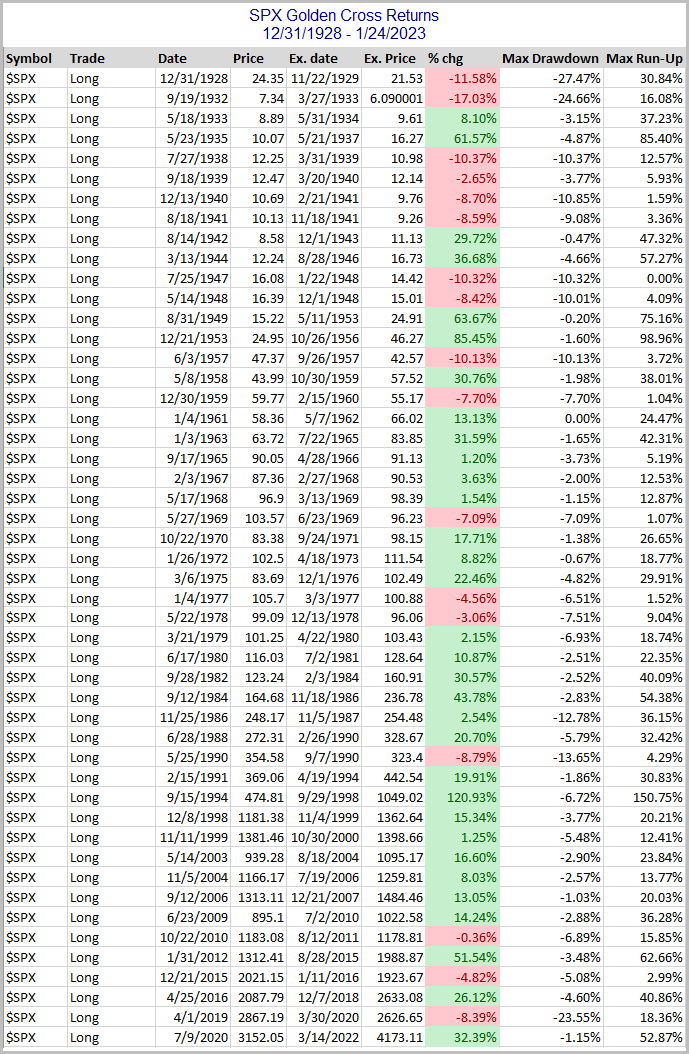

This was a really bullish improvement, as presented by Rob Hanna at Quantifiable Edges within the knowledge under. The S&P 500 index was created in 1958. Utilizing knowledge since that point, the Golden Cross produced optimistic returns 76% of the time as soon as the 50-day fell again under the 200-day. Extra importantly, the drawdown throughout these positive-return intervals by no means exceeded 8.7%. Due to this fact, it comes as no shock that the drawdown after the newest Golden Cross, which occurred at 4,173 on February 2, was a low of three,808 in mid-March. That works out to be 8.7%, which has been adopted by a rebound to greater than 4,100. Will it proceed? The April statistics counsel it’s going to.

Quantifiable Edges

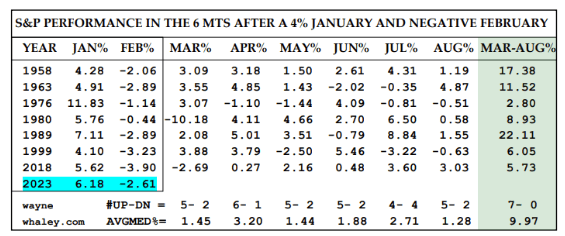

It will get even higher once we contemplate that the S&P 500 posted a achieve of greater than 4% in January, which technical sage Wayne Whaley factors out has resulted in optimistic return within the eight months that adopted in all 21 occurrences since 1950. This January’s achieve of 4% was particular as a result of it was adopted by a loss within the month of February. That has solely occurred eight instances since 1950, and the S&P 500 was greater in all six-month intervals that adopted by a median of roughly 10%.

WayneWhaley.com

This assortment of knowledge in the course of the first quarter doesn’t function the muse for my outlook for a gentle touchdown for the U.S. economic system or new bull marketplace for the S&P 500, however it certain does a fantastic job in reinforcing that outlook. It provides me a whole lot of confidence to say that the bear marketplace for the S&P 500 shall be over sooner slightly than later. I stay in wealth accumulation mode.

{kind=link}