Imgorthand

Introduction

Flowers Meals, Inc. (NYSE:FLO) produces and markets packaged bakery meals merchandise in the USA. Its principal merchandise embrace recent breads, buns, rolls, snack muffins, and tortillas, in addition to frozen breads and rolls below the Nature’s Personal, Dave’s Killer Bread, Marvel, Canyon Bakehouse, Mrs. Freshley’s, and Tastykake model names.

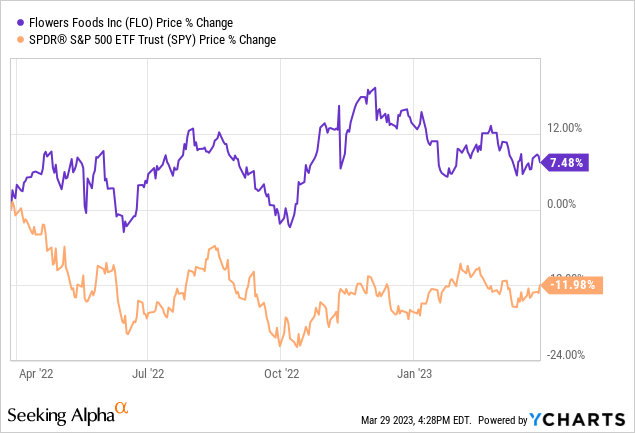

Regardless of the difficult macroeconomic atmosphere up to now 12 months, together with elevated inflation, excessive power costs coupled with excessive transportation prices, together with low shopper confidence ranges, each FLO’s enterprise and inventory has carried out fairly properly. In actual fact, FLO has outperformed the S&P500 by virtually 20% up to now 12 months.

As a result of this outperformance, we’ve got determined to take a more in-depth have a look at FLO’s inventory and its valuation right this moment. We might be utilizing multistage dividend low cost fashions and situation evaluation to find out a spread of truthful values.

The explanations we imagine that the dividend low cost fashions appropriate for the analysis:

- FLO has been paying dividends in every of the previous 19 years, which we imagine is signaling a powerful dedication to returning worth on this kind to shareholders. The agency has additionally managed to extend their dividends in every of the final 9 years. The present annual dividend is $0.88 per share.

- Whereas the present dividend payout ratio is sort of excessive, we imagine that the funds are secure and sustainable because the demand for FLO’s merchandise have remained robust and FLO has additionally demonstrated its skill to shift the associated fee will increase, a minimum of partially, to its clients (each gross sales and earnings have been growing in 2022).

- The enterprise just isn’t immediately influenced by the enterprise cycle or by the patron confidence ranges.

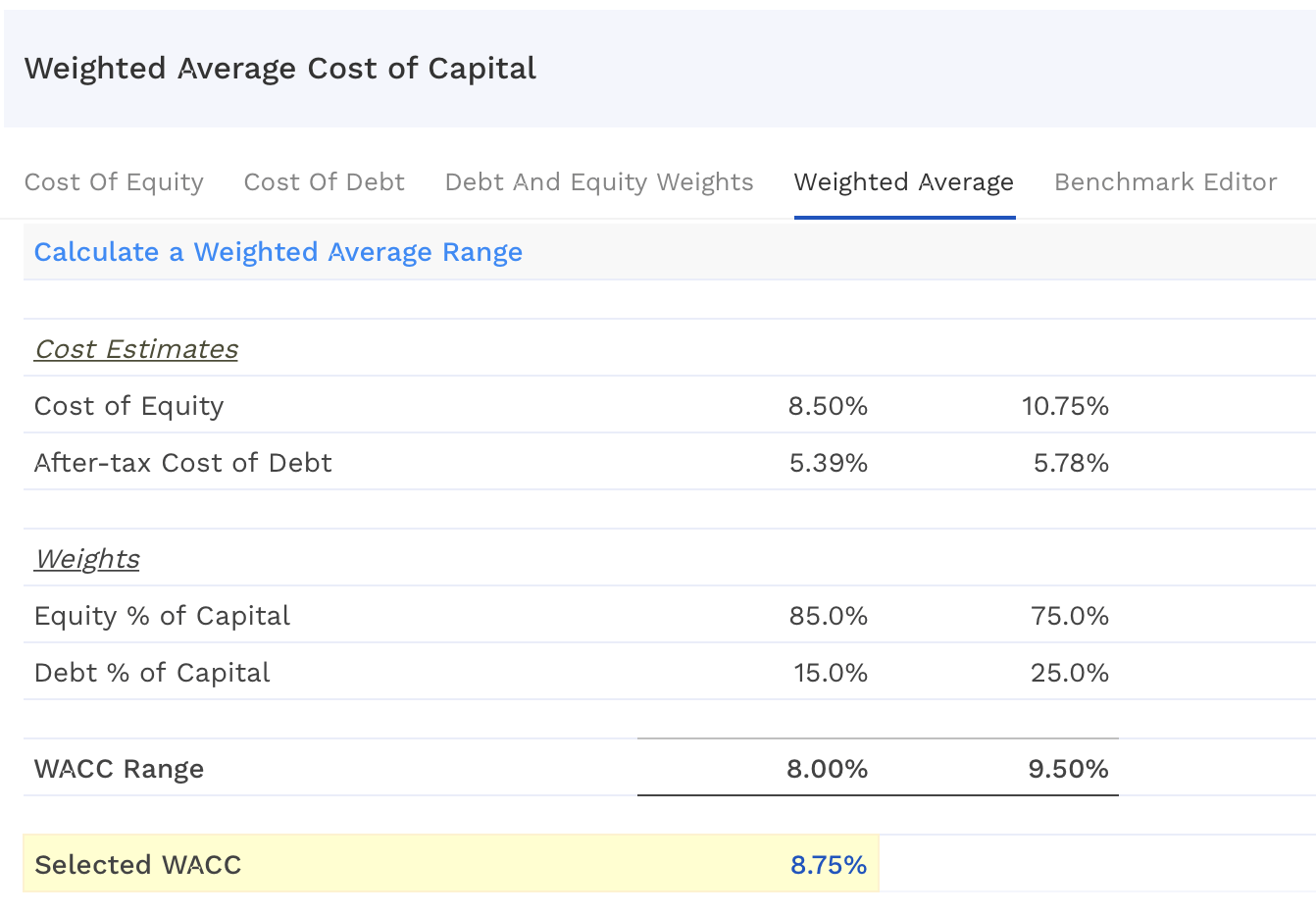

Earlier than we begin evaluating the agency in numerous situations, there’s one assumption that might be legitimate for all our instances, and that’s the assumption of the required fee of return. For evaluation, we might be utilizing a required fee of return of 8.75%, which corresponds to the agency’s weighted common price of capital (WACC).

WACC (finbox.com)

State of affairs 1.

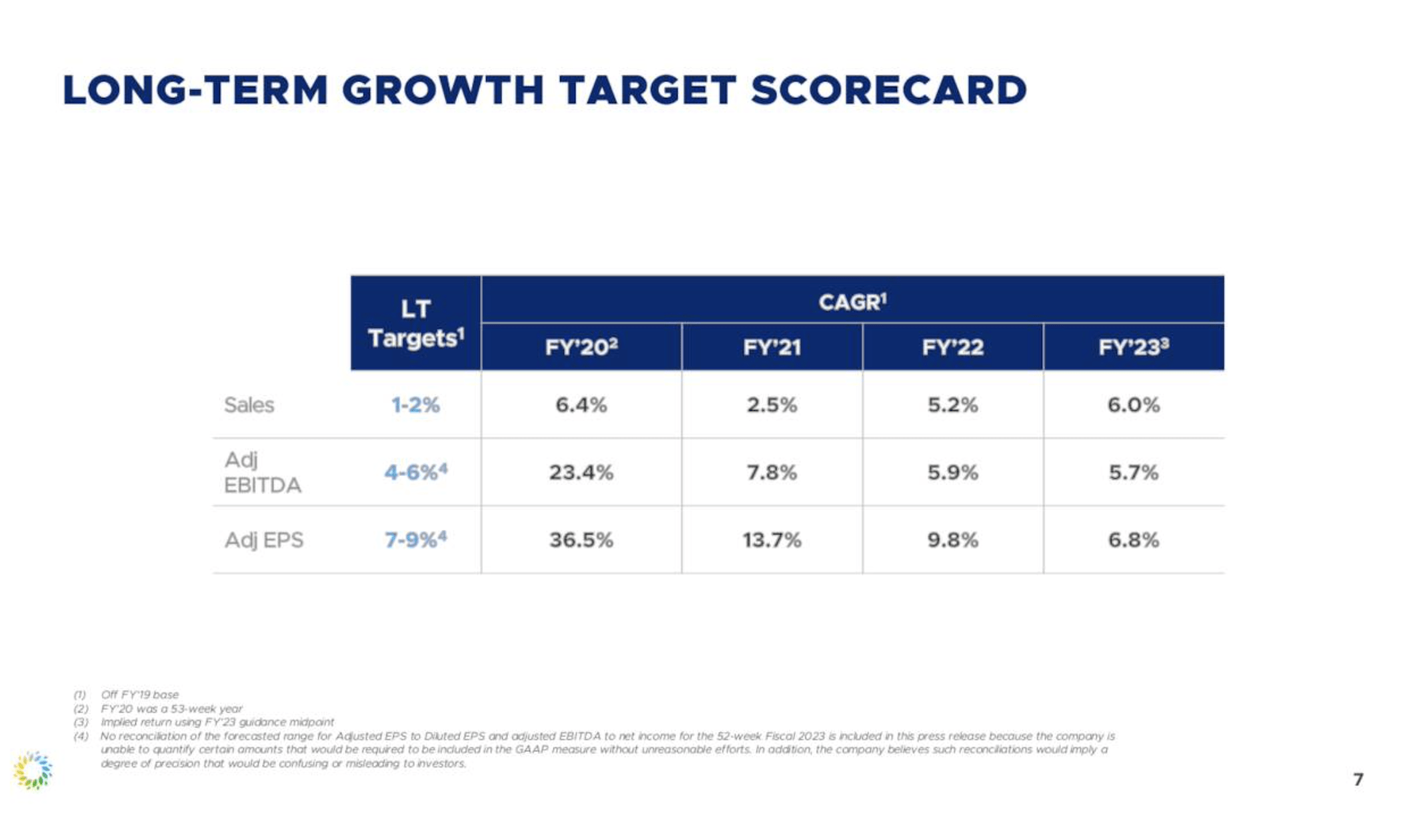

This situation might be based mostly on the agency’s newest long run steerage. They’ve guided for a 6.8% adjusted EPS progress for FY’23.

Progress goal (FLO)

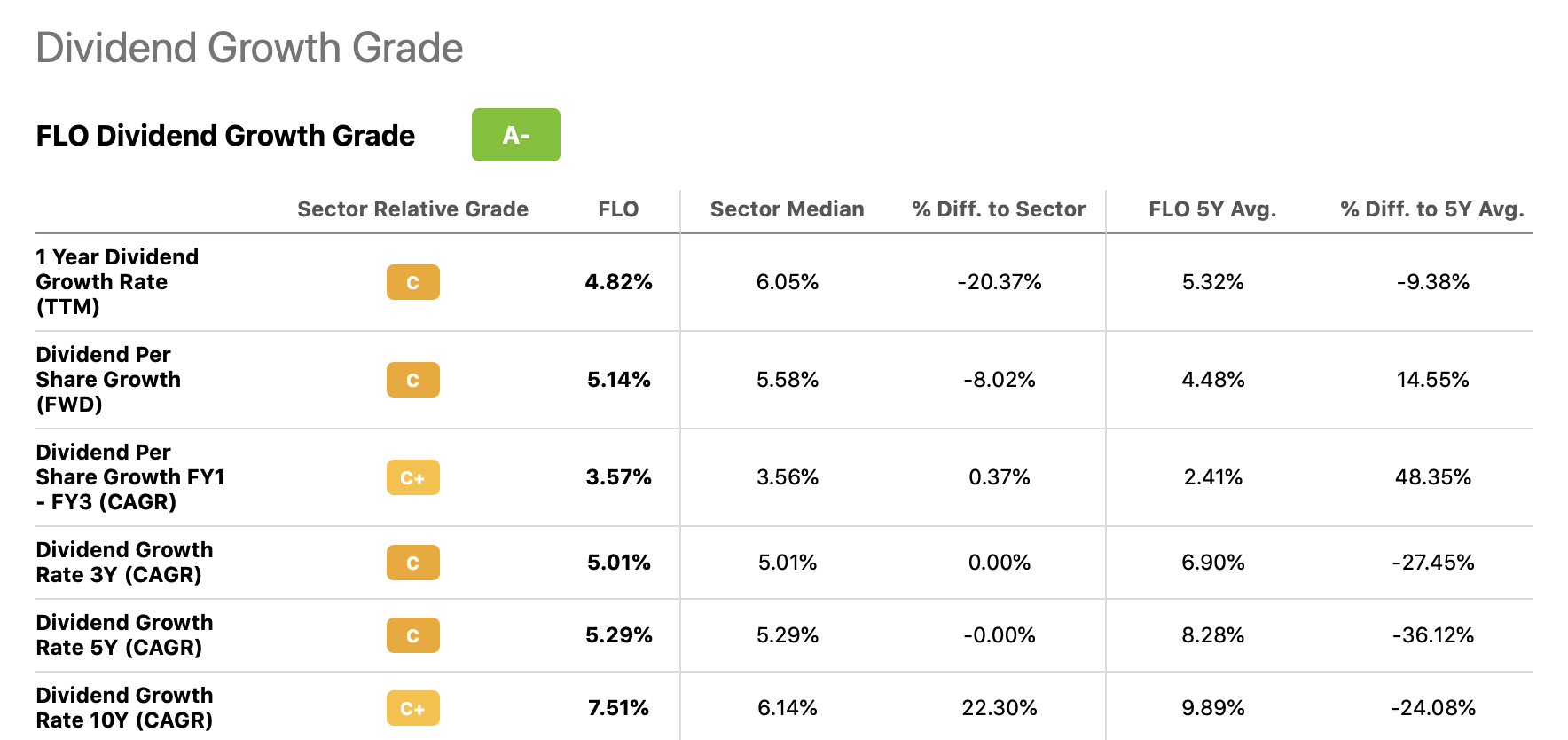

Additionally, the agency has had a 7.5% CAGR of dividends up to now 10 years.

Dividend progress historical past (In search of Alpha)

For these causes, we assume that within the near- and mid-term, the agency will hold growing its dividends at a fee of seven%, and for the long run, we assume a perpetual progress fee of three%, according to the anticipated progress of the general economic system on the whole.

Outcomes (Writer)

Based mostly on these calculations, the truthful worth of the inventory is about $20, representing an about 25% draw back from the present worth ranges.

State of affairs 2.

On this case, we assume that as a result of difficult macroeconomic atmosphere, FLO will solely improve its dividends by 5% within the subsequent 12 months. After that nonetheless, with the potential enchancment of the macroeconomic atmosphere, the dividend would once more begin growing at a fee of seven.5%, according to the agency’s long run common. The perpetual progress fee is once more assumed to be 3%.

Outcomes (Writer)

These calculations additionally point out a good worth near $20 per share.

State of affairs 3.

On this situation, we’re aiming to find out in implied progress fee by the present market worth. Within the close to time period, identical to in situation 1, we might be utilizing a progress fee of seven% within the near- and mid-term. Through the use of the present market worth, we will estimate the implied perpetual progress fee.

Outcomes (Writer)

These calculations point out that the perpetual progress fee priced in by the market is about 4.8%.

Whereas this worth doesn’t appear terribly, particularly as it’s according to the previous 12 months’s dividend progress, it’s fairly a excessive progress fee to be assumed for perpetuity. Don’t forget that adjusting the perpetual progress fee even by small increments can have materials impression on the calculated truthful worth. In our opinion the 4.8% progress in perpetuity is just too excessive.

To sum up

Whereas the agency has proven resilience in difficult macroeconomic environments, together with growing gross sales and EPS, we imagine that the agency is barely overpriced based mostly on its dividends.

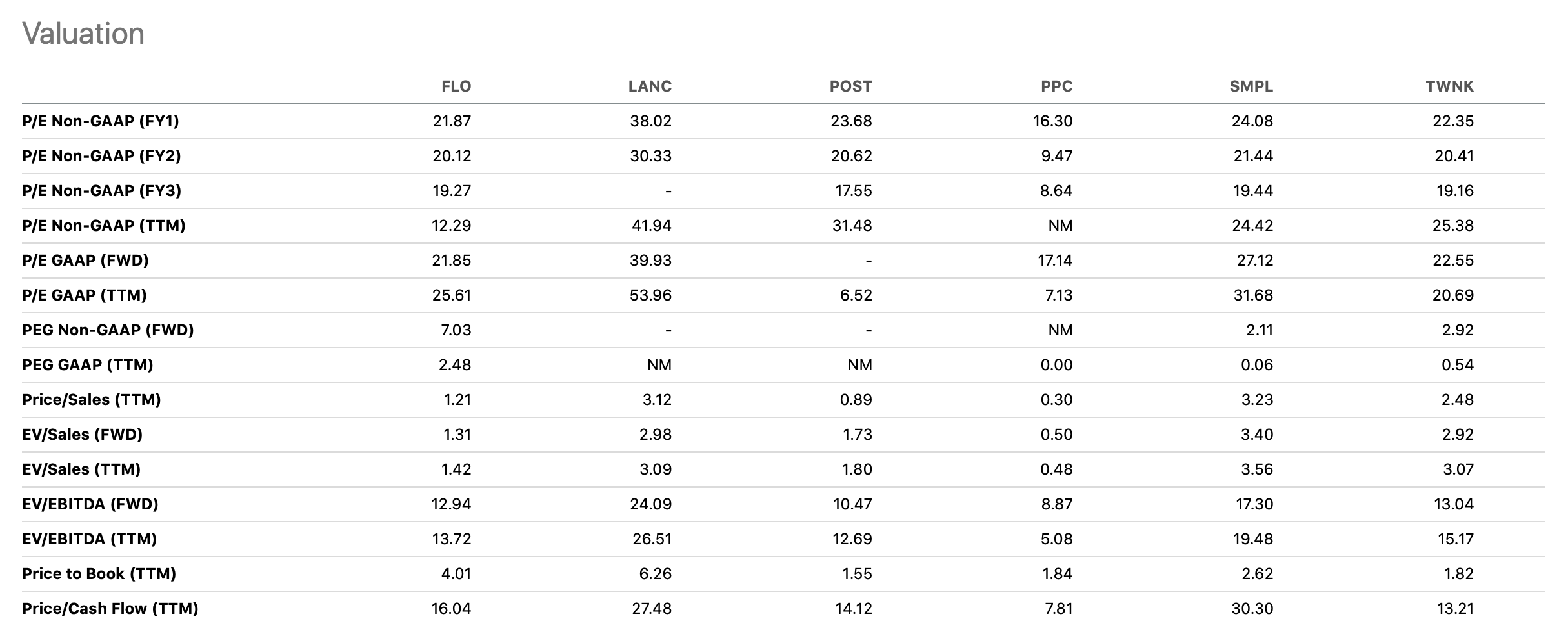

Then again, the agency seems to be valued roughly according to most of its friends and rivals, based mostly a number of conventional worth multiples.

Comparability (In search of Alpha)

For these causes, we at the moment assign a impartial ranking to FLO’s inventory.

Imgorthand

Introduction

Flowers Meals, Inc. (NYSE:FLO) produces and markets packaged bakery meals merchandise in the USA. Its principal merchandise embrace recent breads, buns, rolls, snack muffins, and tortillas, in addition to frozen breads and rolls below the Nature’s Personal, Dave’s Killer Bread, Marvel, Canyon Bakehouse, Mrs. Freshley’s, and Tastykake model names.

Regardless of the difficult macroeconomic atmosphere up to now 12 months, together with elevated inflation, excessive power costs coupled with excessive transportation prices, together with low shopper confidence ranges, each FLO’s enterprise and inventory has carried out fairly properly. In actual fact, FLO has outperformed the S&P500 by virtually 20% up to now 12 months.

As a result of this outperformance, we’ve got determined to take a more in-depth have a look at FLO’s inventory and its valuation right this moment. We might be utilizing multistage dividend low cost fashions and situation evaluation to find out a spread of truthful values.

The explanations we imagine that the dividend low cost fashions appropriate for the analysis:

- FLO has been paying dividends in every of the previous 19 years, which we imagine is signaling a powerful dedication to returning worth on this kind to shareholders. The agency has additionally managed to extend their dividends in every of the final 9 years. The present annual dividend is $0.88 per share.

- Whereas the present dividend payout ratio is sort of excessive, we imagine that the funds are secure and sustainable because the demand for FLO’s merchandise have remained robust and FLO has additionally demonstrated its skill to shift the associated fee will increase, a minimum of partially, to its clients (each gross sales and earnings have been growing in 2022).

- The enterprise just isn’t immediately influenced by the enterprise cycle or by the patron confidence ranges.

Earlier than we begin evaluating the agency in numerous situations, there’s one assumption that might be legitimate for all our instances, and that’s the assumption of the required fee of return. For evaluation, we might be utilizing a required fee of return of 8.75%, which corresponds to the agency’s weighted common price of capital (WACC).

WACC (finbox.com)

State of affairs 1.

This situation might be based mostly on the agency’s newest long run steerage. They’ve guided for a 6.8% adjusted EPS progress for FY’23.

Progress goal (FLO)

Additionally, the agency has had a 7.5% CAGR of dividends up to now 10 years.

Dividend progress historical past (In search of Alpha)

For these causes, we assume that within the near- and mid-term, the agency will hold growing its dividends at a fee of seven%, and for the long run, we assume a perpetual progress fee of three%, according to the anticipated progress of the general economic system on the whole.

Outcomes (Writer)

Based mostly on these calculations, the truthful worth of the inventory is about $20, representing an about 25% draw back from the present worth ranges.

State of affairs 2.

On this case, we assume that as a result of difficult macroeconomic atmosphere, FLO will solely improve its dividends by 5% within the subsequent 12 months. After that nonetheless, with the potential enchancment of the macroeconomic atmosphere, the dividend would once more begin growing at a fee of seven.5%, according to the agency’s long run common. The perpetual progress fee is once more assumed to be 3%.

Outcomes (Writer)

These calculations additionally point out a good worth near $20 per share.

State of affairs 3.

On this situation, we’re aiming to find out in implied progress fee by the present market worth. Within the close to time period, identical to in situation 1, we might be utilizing a progress fee of seven% within the near- and mid-term. Through the use of the present market worth, we will estimate the implied perpetual progress fee.

Outcomes (Writer)

These calculations point out that the perpetual progress fee priced in by the market is about 4.8%.

Whereas this worth doesn’t appear terribly, particularly as it’s according to the previous 12 months’s dividend progress, it’s fairly a excessive progress fee to be assumed for perpetuity. Don’t forget that adjusting the perpetual progress fee even by small increments can have materials impression on the calculated truthful worth. In our opinion the 4.8% progress in perpetuity is just too excessive.

To sum up

Whereas the agency has proven resilience in difficult macroeconomic environments, together with growing gross sales and EPS, we imagine that the agency is barely overpriced based mostly on its dividends.

Then again, the agency seems to be valued roughly according to most of its friends and rivals, based mostly a number of conventional worth multiples.

Comparability (In search of Alpha)

For these causes, we at the moment assign a impartial ranking to FLO’s inventory.

{kind=link}