JJFarquitectos/iStock Editorial by way of Getty Photos

CaixaBank (OTCPK:CAIXY) is an fascinating play for earnings traders resulting from its high-dividend yield and low cost valuation.

Firm Overview

CaixaBank is among the many largest banks in Spain, with a nationwide presence, and greater than 20 million prospects on the finish of 2022. Its core enterprise is retail and industrial banking, whereas the financial institution additionally affords different monetary companies and merchandise, similar to insurance coverage, mutual funds, past others.

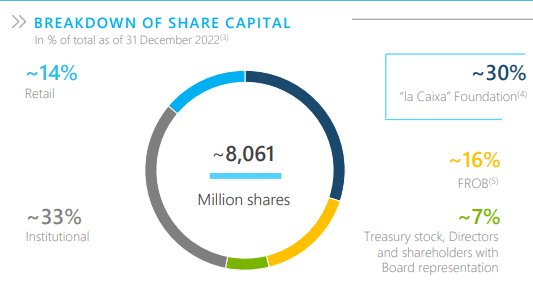

Its present market worth is about $28 billion, being subsequently a mid-sized financial institution in Europe by this measure. It trades within the U.S. on the over-the-counter market, however traders ought to notice that its shares have significantly better liquidity in its home itemizing. The financial institution’s largest shareholder is La Caixa Basis, with a stake of about 30%.

Share capital (CaixaBank)

Enterprise Profile & Progress

CaixaBank is the biggest retail financial institution in Spain, holding a market share of about 24% in loans and 25% in deposits. It additionally has the biggest retail department community, holding greater than 3,800 branches all through the nation. On the finish of 2022, its mortgage guide amounted to some €360 billion, whereas its complete steadiness sheet was near €600 billion. Its enterprise profile is properly diversified throughout banking, insurance coverage, asset administration, and shopper finance.

Past its robust place within the Spanish banking market, the place it holds market shares between 20-30% for the overwhelming majority of banking merchandise, CaixaBank additionally has a world operation in Portugal, by way of its fully-owned financial institution Banco BPI. In Portugal, it holds market share of about 11% for an important banking merchandise, being among the many 4 largest banks within the nation.

Whereas previously CaixaBank held important stakes in different banks and enormous Spanish corporates, its technique in recent times has been to promote these stakes and focus its enterprise on its core operations, a transfer that is sensible in my view and results in a extra easy enterprise profile that’s simpler to worth for minority shareholders. Because of this CaixaBank’s present funding case is totally geared to banking, whereas previously an excellent a part of its fairness worth got here from its earlier stakes in Repsol (OTCQX:REPYY) and Telefonica (TEF), which was a enterprise profile extra just like an funding firm relatively than a financial institution.

Furthermore, from a capital standpoint, these fairness stakes had been fairly expensive for the financial institution, because the risk-weighted property assigned to fairness stakes is 290%, which implies CaixaBank wanted to allocate numerous capital to those stakes. By promoting them, it was additionally capable of allocate capital to its core operations, and obtain the next return on fairness.

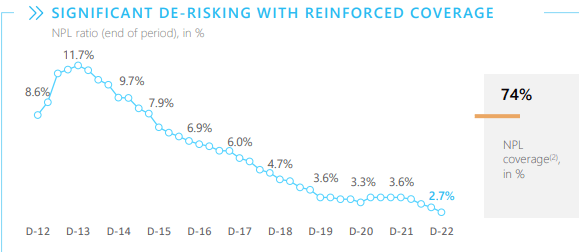

Relating to its steadiness sheet, its technique has been to de-risk its threat profile by promoting riskier mortgage positions and non-performing property over the previous few years. This has been an extended course of and its non-performing mortgage (NPL) ratio remains to be above the European banking sector common, however the pattern continues to maneuver in the fitting course and NPLs ought to proceed to lower, except the Spanish financial system enters right into a extreme recession within the close to future.

NPL ratio (CaixaBank)

Regardless that CaixaBank has made a number of acquisitions over the previous few years, its development technique is especially natural, pushing for digitalization to supply a greater customer support, whereas lowering prices and complexity on the similar time. Relating to acquisitions, the financial institution isn’t reportedly looking for to develop its worldwide footprint, thus it might purchase smaller opponents in its home market if the chance arises, and if it is sensible from a monetary perspective.

Monetary Overview

Relating to its monetary efficiency, CaixaBank has delivered a optimistic working efficiency in recent times, supported by a positive financial atmosphere in Spain and Portugal, and extra lately by rising rates of interest in Europe that are a robust tailwind for its revenues.

Certainly, over the past year, CaixaBank’s revenues had been boosted by greater volumes and rates of interest, resulting in an annual development of 5.5% to €11.6 billion.

Its mortgage guide elevated by 2.4% YoY, which is optimistic for income development, however what had probably the most impression had been greater rates of interest, with web curiosity earnings rising by 7.7% YoY, to €6.9 billion. Its charges and commissions earnings elevated 3.3% YoY to greater than €5 billion, supported by insurance coverage merchandise that had been capable of offset some weak spot in asset administration.

Relating to prices, the financial institution confirmed superb price administration, having the ability to report complete bills of €6 billion within the yr, a decline of 5.6% YoY. This resulted in an enchancment in effectivity, measured by its cost-to-income ratio of 52%. Whereas this effectivity stage is suitable throughout the European banking sector, it’s greater than in comparison with its peer BBVA (BBVA) as an illustration which had a cost-to-income ratio of 44% in 2022, displaying that CaixaBank nonetheless has room to additional enhance effectivity and obtain greater earnings development within the coming years.

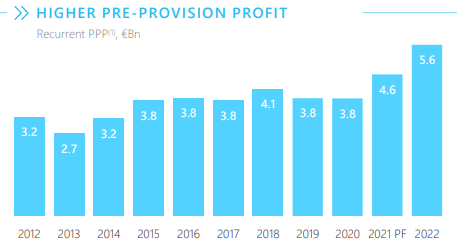

Regardless of that, CaixaBank’s working revenue has grown significantly over the previous couple of years, because the financial institution was capable of report optimistic working jaws (income development greater than price development), a pattern that’s prone to keep within the coming quarters as rates of interest proceed to maneuver greater in Europe.

Pre-provision revenue (CaixaBank)

Relating to provisions, CaixaBank has been capable of report a steady price of threat over the previous couple of years at 25 foundation factors (bps) of complete loans, displaying that its credit score high quality is sweet. Nonetheless, given rising rates of interest and a slowdown in financial exercise, it’s seemingly that credit score high quality might deteriorate within the subsequent few quarters. Because of this provisions for mortgage losses might improve in 2023, which is a headwind for earnings development, although there isn’t to this point a lot proof of a big drop in credit score high quality.

As a consequence of a mixture of upper revenues, decrease bills, and steady provisions, CaixaBank’s bottom-line elevated to greater than €3.1 billion in 2022, up by 29.7% YoY. Its return on tangible fairness ratio, a key measure of profitability throughout the banking sector, was 9.8% (plus 2.6 proportion factors in comparison with 2021).

Going ahead, the financial institution is geared to greater rates of interest in Europe, because the European Central Financial institution has hiked in latest months and its steering is for a couple of extra hikes within the close to future, which bodes properly for the financial institution’s web curiosity earnings. However, credit score high quality is the foremost uncertainty that may have an effect on its profitability, being subsequently a key measure to watch in its upcoming earnings launch.

Capital & Dividends

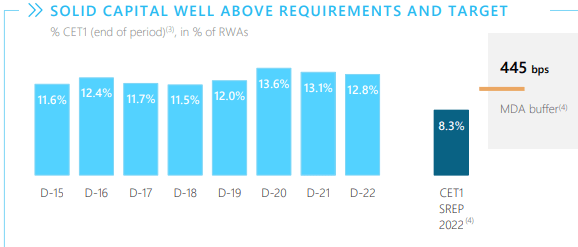

Relating to its capitalization, CaixaBank has an excellent capitalization measured by its core fairness tier 1 (CET1) ratio of 12.8% on the finish of 2022. This stage is in-line with the common of the European banking sector, however decrease than in comparison with the very best capitalized banks in Europe, however given CaixaBank’s retail-oriented enterprise mannequin it’s a lot greater than its capital requirement. Certainly, its capital requirement was solely 8.3% in 2022, displaying that its capital buffer is kind of substantial and offers a strong place to distribute extra capital to shareholders.

Capital (CaixaBank)

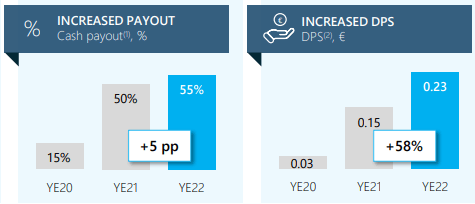

Certainly, CaixaBank’s shareholder remuneration coverage has been enticing lately, because the financial institution elevated its annual dividend in a big manner. Its final annual dividend, associated to 2022 earnings and anticipated to be distributed subsequent month, was set at €0.23 per share (up by 58% YoY) and its dividend payout ratio additionally elevated from 50% of earnings, to 55% of its revenue final yr.

Dividends (CaixaBank)

At its present share worth, CaixaBank’s dividend yield is shut to six.5%, which is kind of enticing to earnings traders. Furthermore, the financial institution additionally carried out share repurchases of €1.8 billion over the last yr, additional enhancing its capital return coverage.

On condition that CaixaBank has an excellent capital place and doesn’t have to retain a lot earnings within the quick to medium time period, its goal is to distribute extra capital above a CET1 ratio of 12%, each by way of dividends and share buybacks. It has already distributed €3.5 billion throughout 2022, which implies that it nonetheless has some €5.5 billion to distribute throughout 2023-24, to achieve its three-year goal of €9 billion.

Its steering is to distribute between 50-60% of annual income by way of dividends, thus CaixaBank ought to ship a rising dividend over the subsequent two years and carry out additional share buybacks. Certainly, in keeping with analysts’ estimates, its dividend is anticipated to extend to €0.29 per share by 2024, which might push its dividend yield to greater than 8% at its present share worth.

Conclusion

CaixaBank is a financial institution with strong fundamentals and its working efficiency is optimistic, supported largely by rising rates of interest. Regardless of this background, it’s at present trading at solely 0.78x guide worth, at a reduction to the European banking sector, and affords a high-dividend yield that’s sustainable. Thus, CaixaBank is a compelling earnings play proper now, being an excellent alternative for long-term traders to get an excellent entry worth following the latest weak spot in financial institution shares resulting from woes in U.S. regional banks and the Credit score Suisse (CS) saga.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}