grandriver

EOG Assets (NYSE:EOG) is among the largest oil and fuel corporations on this planet with a market capitalization of greater than $60 billion. The corporate’s robust belongings usually trades at a premium valuation however with its latest 30% drop, we see that as a novel funding alternative that we advocate benefiting from.

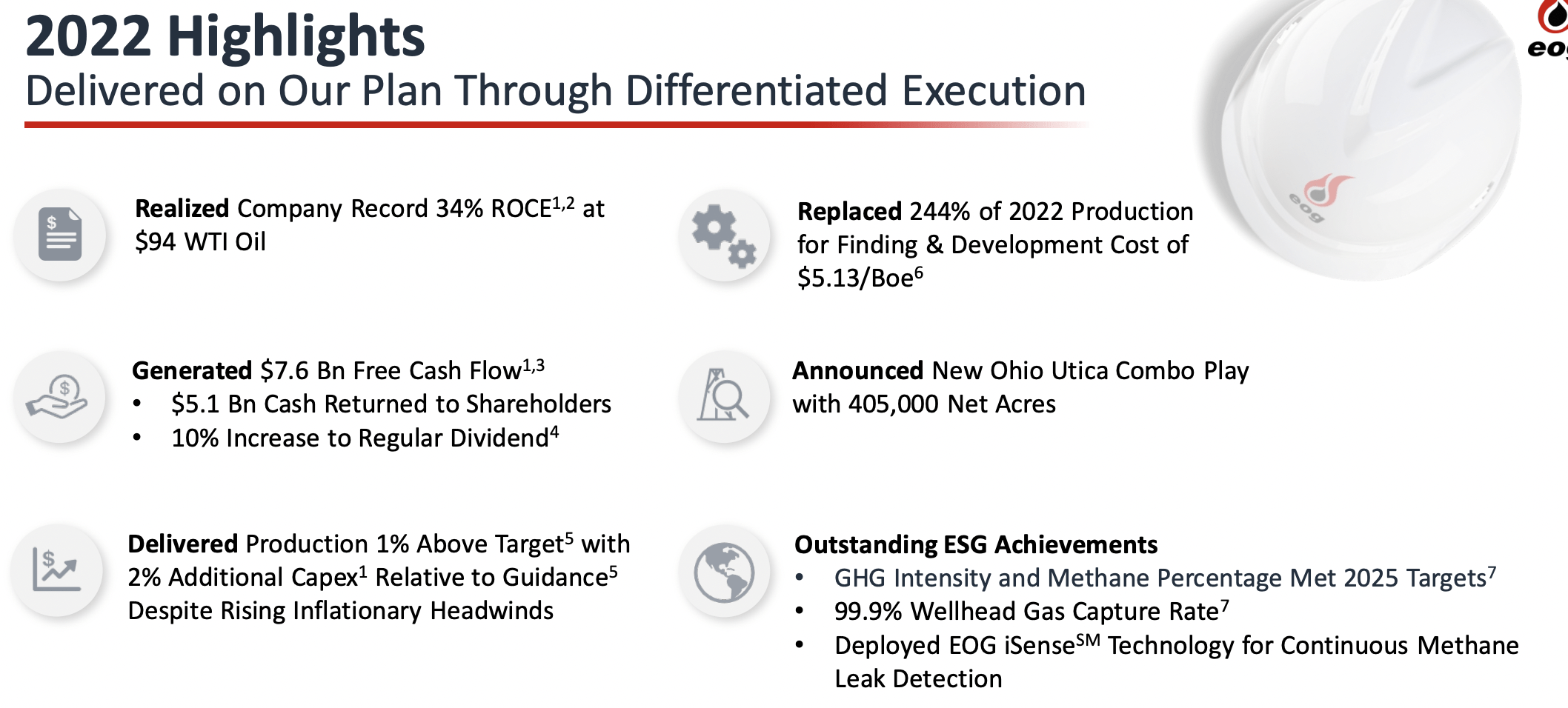

EOG Assets 2022 Efficiency

EOG Assets had a robust 2022, highlighting its general asset power.

EOG Assets Investor Presentation

EOG Assets generated an enormous 34% ROCE at $94 WTI. $7.6 billion in FCF resulted in $5.1 billion being returned to shareholders via repurchases and particular dividends, together with a ten% improve in common dividends. The corporate delivered manufacturing 1% above targets with 2% extra capex.

Most significantly the corporate changed 244% of its manufacturing with an F&D value at a mere $5.13 / barrel. The corporate’s new Ohio Utica Combo play has 405 thousand acres. The corporate had a blowout 12 months, clearly highlighting the extremely robust upside that is obtainable within the firm’s enterprise when crude costs common greater.

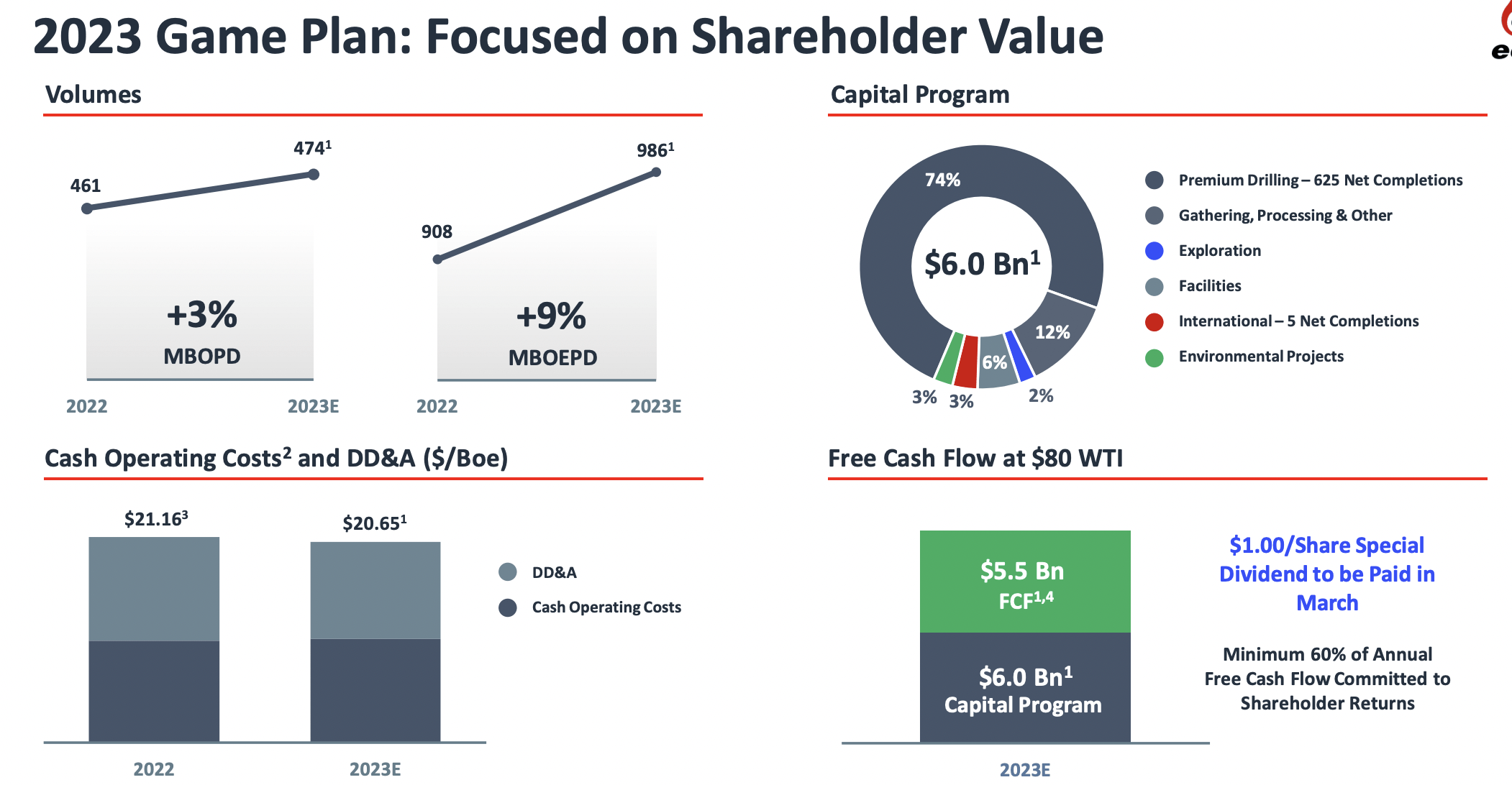

EOG Assets 2023 Plan

EOG Assets has a robust plan in 2023, though it could possibly be closely affected by decrease oil costs.

EOG Assets Investor Presentation

The corporate’s 2023 recreation plan assumes $80 WTI and proper now that is wanting like a toss-up. China reopening may add substantial demand, nevertheless, an incapacity for the FED to attain a smooth touchdown may additionally damage costs considerably. We actually see it as a toss-up to see the place oil costs end for the calendar 12 months.

Nonetheless, the corporate’s numbers are robust. With a big $6 billion capital program, it expects money working prices + DD&A to be a hair decrease than $20.65 / barrel. That is spectacular in an inflationary surroundings. The corporate expects manufacturing to extend by an enormous 9% in MBOEPD, approaching 1 million barrels / day.

That signifies that ought to oil costs drop additional, the corporate has room to lower capital spending with impartial manufacturing.

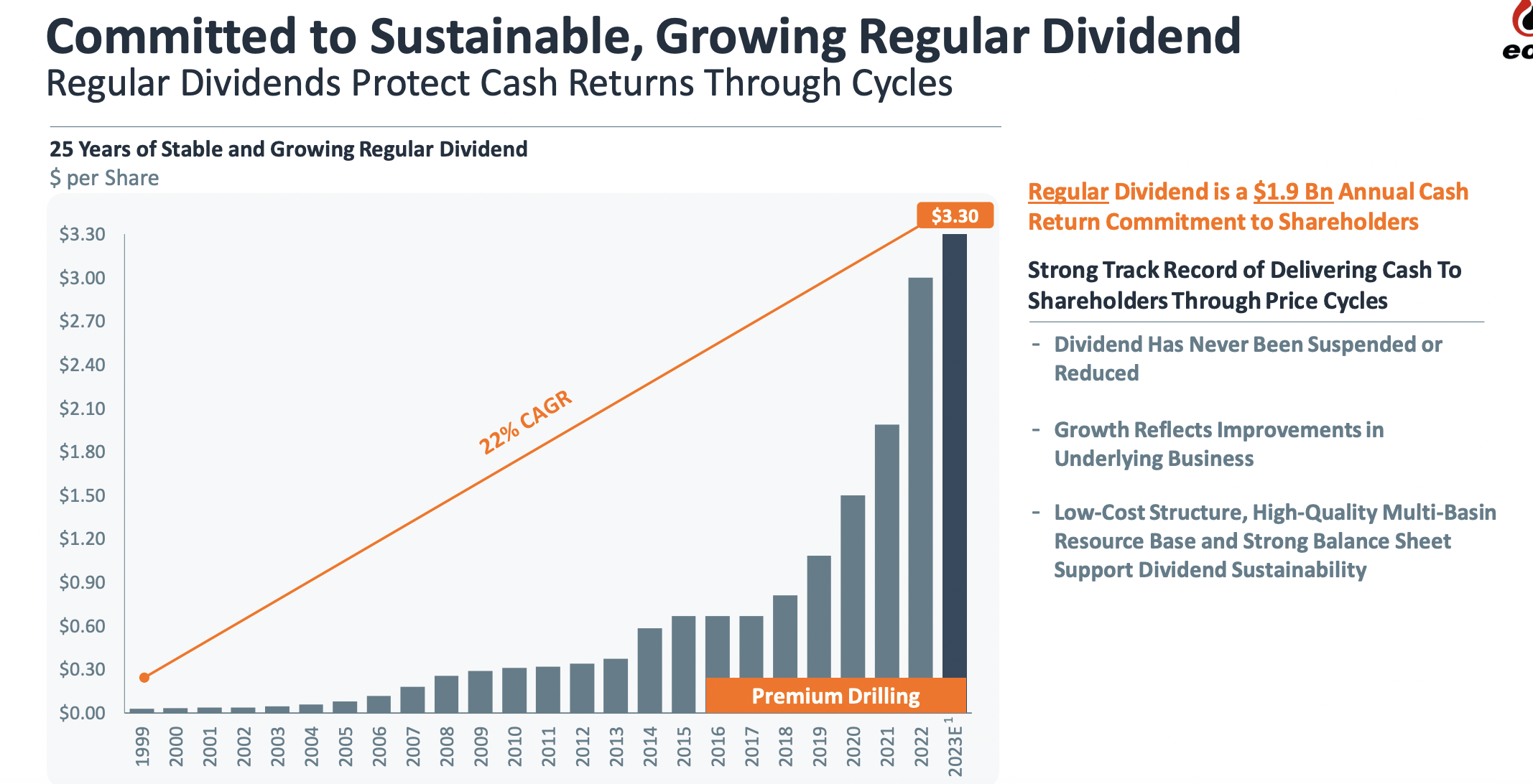

EOG Assets Dividend

The corporate stays dedicated to each its dividend and general shareholder returns.

EOG Assets Investor Presentation

The corporate’s dividend has grown by 22% annualized as the corporate has quickly elevated its deal with premium drilling. The present base dividend is 3.1%, nevertheless, the corporate has augmented it considerably with particular dividends as a part of its return plan. The corporate has a robust observe report of will increase through the downturn and we anticipate that to proceed.

On the identical time the corporate has a $5 billion buyback authorization which we would prefer to see it benefit from if share costs drop additional. The corporate’s complete particular dividends up to now have been $5.1 billion, which is greater than 8% of particular dividends.

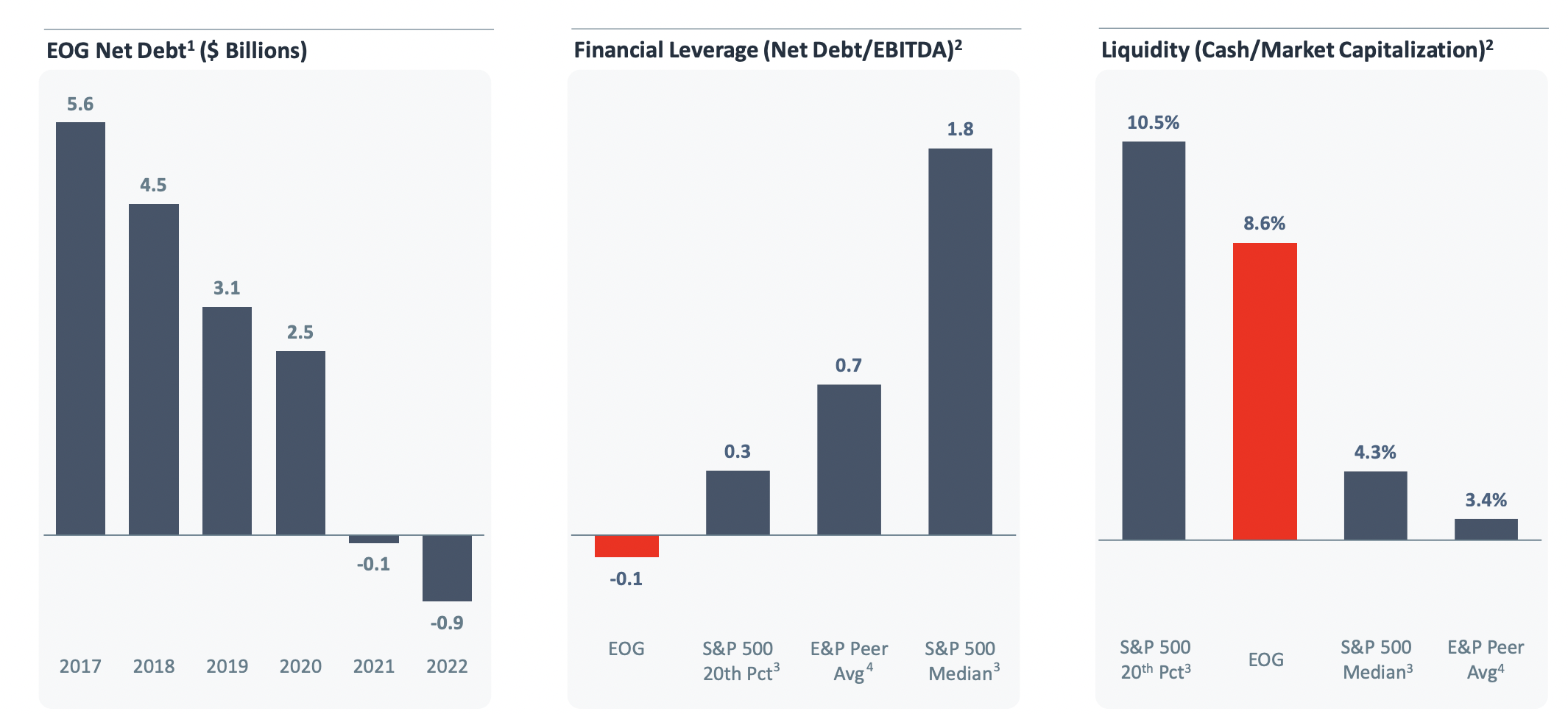

EOG Assets Debt

The corporate’s steadiness sheet and debt will allow continued shareholder returns.

EOG Assets Investor Presentation

The corporate has one of many strongest steadiness sheets within the trade. It has -$0.9 billion in web debt (i.e. a web money place) one thing that highlights not solely the power of its steadiness sheet however provides it one of many strongest steadiness sheets within the trade. The corporate has robust liquidity meaning it may possibly opportunistically use money when obtainable to drive elevated returns.

In reality, ought to the downturn improve additional, we would prefer to see the corporate have a look at some opportunistic acquisitions to help its portfolio.

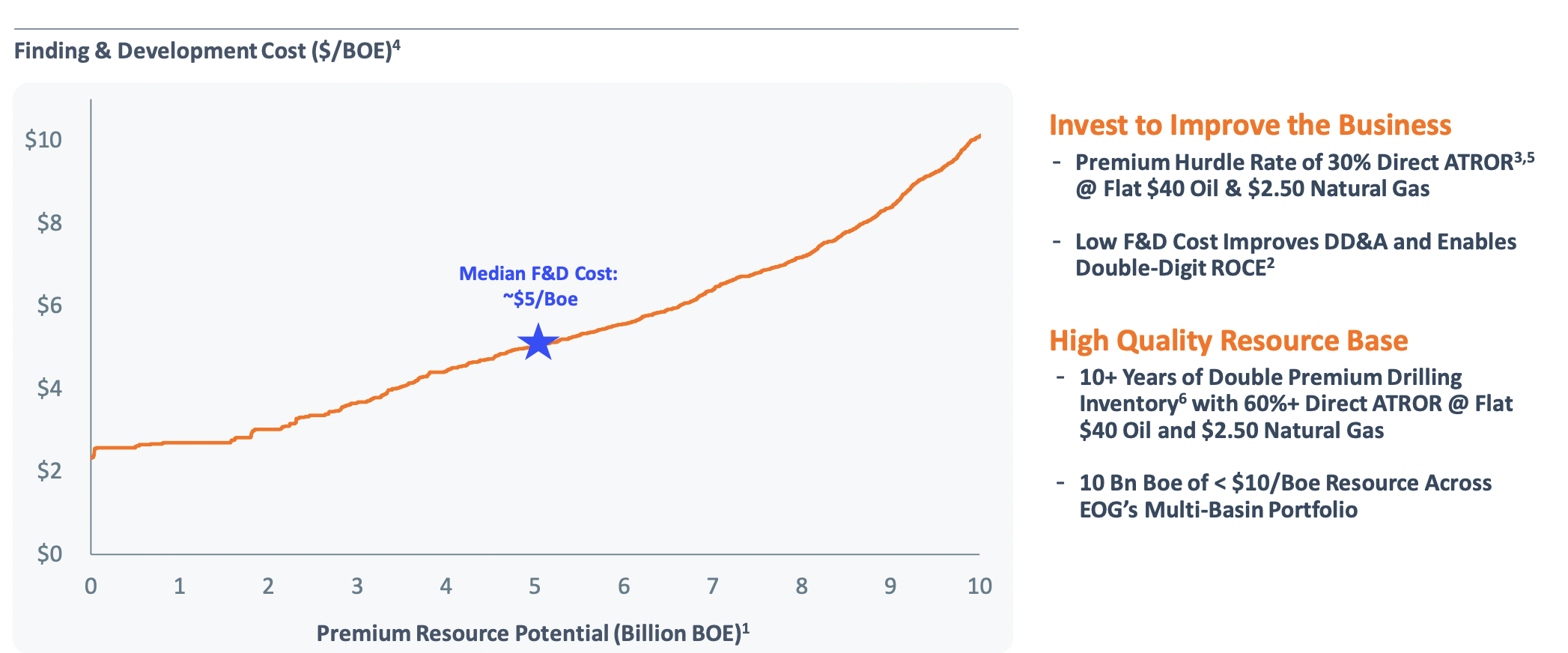

EOG Assets Progress and Margins

EOG Assets is concentrated on aggressively discovering new belongings with a low breakeven.

EOG Assets Investor Presentation

The corporate’s median F&D value of a mere $5/barrel is extremely robust. The corporate has a robust hurdle of 30% ATROR at $40 oil / $2.5 pure fuel. The corporate’s new deal with premium drilling has been maintainable via robust reserve replacements and the present stock is 10+ years of what the corporate calls its double premium drilling wells.

The corporate sees 10 billion of potential <$10/barrel assets throughout its multi-basin portfolio, equal to virtually 30-years of manufacturing. We anticipate the corporate to proceed increasing its reserves.

Our View

EOG Assets is a premium firm that wants greater costs and a better valuation to justify its share worth.

EOG Assets Investor Presentation

The corporate has a $62 billion valuation which is definitely a reasonably robust valuation. The corporate generated $7.6 billion in FCF in 2022, however that is simple once you’re realizing a worth of $94 WTI. At $80 WTI, the corporate’s forecast is for $5.5 billion in FCF simply after a $6 billion capital program, which represents a 9% FCF yield.

For perspective, present WTI costs are $70 / barrel. There’s quite a lot of weak spot within the economic system that would end in costs dropping additional, decreasing the corporate’s money move into mid single-digits. Nonetheless, there’s one thing to be mentioned concerning the firm’s extremely robust belongings and low breakeven positioning that it has.

Thesis Threat

The biggest threat to the thesis is crude oil costs. Costs are already $10 / barrel earlier than the corporate’s plan for $80 WTI. The corporate’s hefty $6 billion capital plan, anticipated to end in virtually 10% manufacturing progress, means its remaining FCF is far more inclined to a worth downturn. Nonetheless, with no web debt it may possibly climate loads.

Conclusion

EOG Assets is a premium firm buying and selling at a premium valuation. The corporate has no web debt and it is planning to spend $6 billion in capital spending for 2023 to extend its oil equal manufacturing by virtually 10%. Nonetheless, that use of capital spending signifies that the corporate’s remaining FCF is extra inclined to crude oil costs.

The corporate has a core dividend of simply over 3% that it may possibly comfortably afford. Its utilized particular dividends and share repurchases previously and we anticipate the corporate will try this as effectively. Nonetheless, with main potential volatility going into the tip of 12 months, the corporate is inclined to what costs do. Regardless, it is a robust firm with robust financials, and in consequence, we advocate investing.

{kind=link}