pong6400

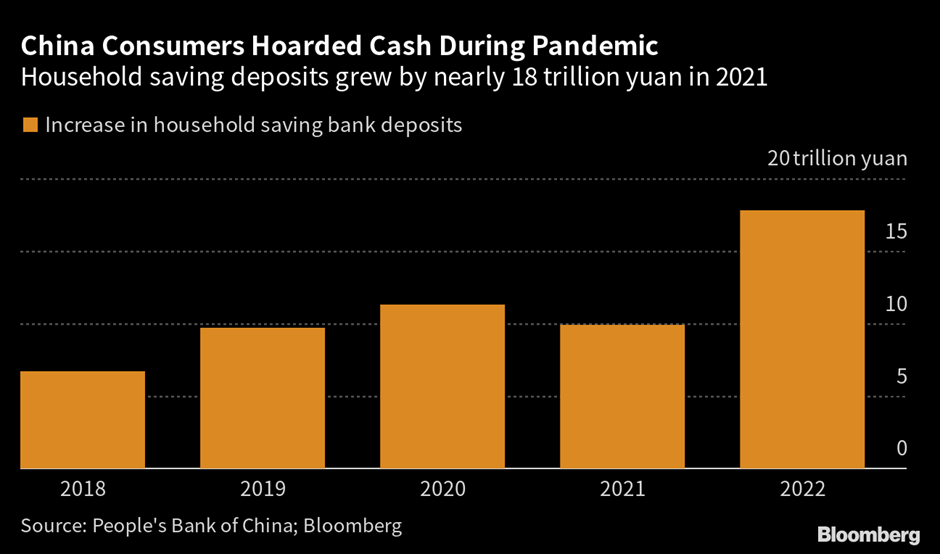

China seems to be poised to be the one main financial system to see an acceleration of GDP progress this 12 months amid a post-COVID restoration led by home demand. With cash provide progress additionally accelerating amid a rebound in key financial information factors (e.g., PMI and retail gross sales numbers), the near-term setup for Chinese language equities stays compelling. The unwinding of the huge family deposit build-up throughout the COVID-impacted years can be one other key tailwind all year long as family incomes recuperate and capital is reallocated into riskier property. To capitalize on a possible rebound, I’d favor an allocation to funds with increased home consumer-based publicity vs. externally derived revenue streams. Given its consumer-focused allocation, the Templeton Dragon Fund (NYSE:TDF) is a good choose inside the actively managed universe; the flexibleness to rotate its asset allocation (e.g., A-shares vs. US-listed ADRs) to mitigate geopolitical dangers is a bonus.

Fund Overview – Actively Managed, Shopper-Targeted Chinese language Publicity

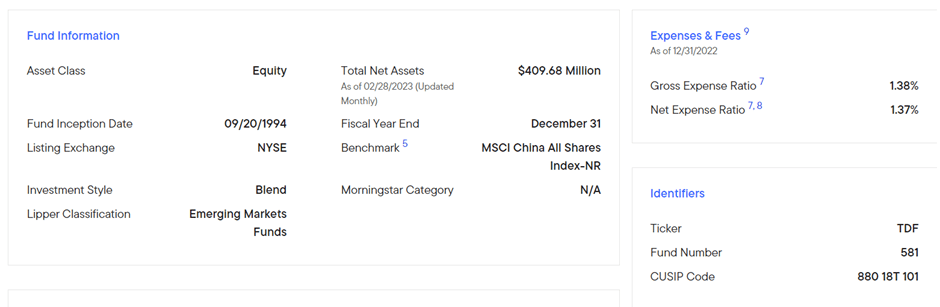

The NYSE-listed Templeton Dragon Fund seeks to ship long-term capital appreciation by investing >45% of its property in Chinese language equities. The fund’s benchmark is the MSCI China All Shares Index, which tracks massive and mid-cap Chinese language equities throughout share lessons in Hong Kong, Shanghai, Shenzhen, and past. The ETF held $410m of web property on the time of writing and charged a 1.4% expense ratio (gross and web), inserting it on the decrease finish of comparable actively managed China obtainable to US buyers. Key information on the ETF is as per the graphic beneath:

Templeton

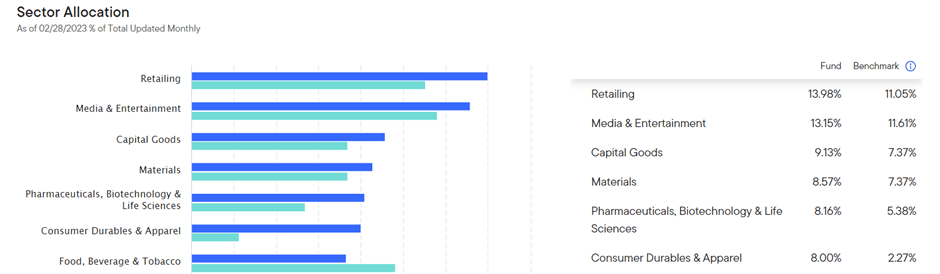

As mirrored within the chart beneath, the fund maintains an obese on the Chinese language shopper, with Retailing (14.0% vs. 11.1% benchmark) and Media & Leisure (13.2% vs. 11.6% benchmark) main the best way. Shopper Durables & Attire is the biggest obese by %pt at 8.0% in comparison with 2.3% for the benchmark, reflecting the fund’s leverage to a consumer-led rebound. Rounding out the top-five sectors are Capital Items (9.1%), Supplies (8.6%), and Prescription drugs, Biotechnology & Life Sciences (8.2%). In complete, the top-five sectors accounted for 53.0% of the overall portfolio.

Templeton

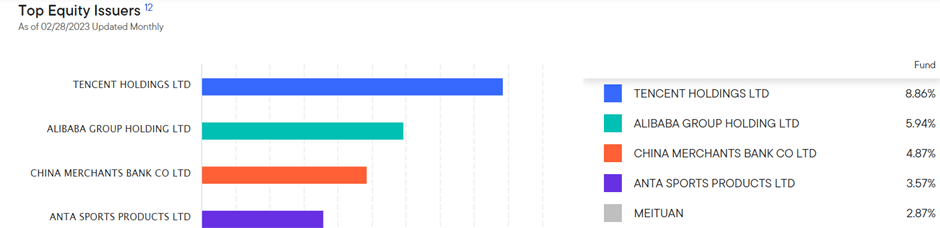

The fund’s largest single-stock holdings are Chinese language tech and leisure large Tencent Holdings (OTCPK:TCEHY) (8.9%), Chinese language e-commerce chief Alibaba Group (BABA) (5.9%), industrial banking chief China Retailers Financial institution (OTCPK:CIHKY) (4.9%), Chinese language sports activities gear firm ANTA Sports activities (OTCPK:ANPDY) (3.6%) and Chinese language buying platform Meituan (OTCPK:MPNGF) (2.9%). The portfolio consists of 67 holdings (vs. 789 for the benchmark index), with the highest 5 holdings accounting for ~26% of the general portfolio. Of observe, the fund is primarily made up of H/A shares, so buyers involved about regulatory dangers related to abroad listings (e.g., US-listed ADRs) might choose China publicity by way of TDF.

Templeton

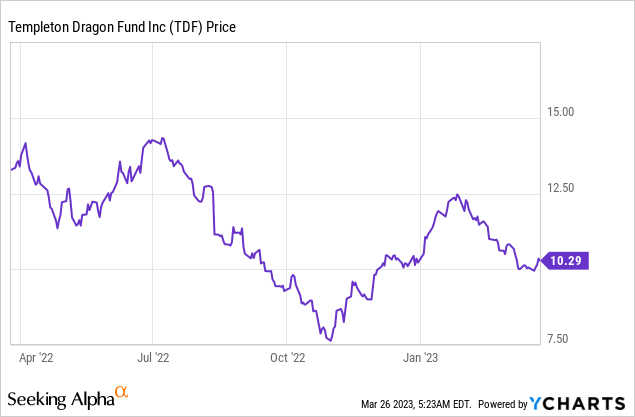

On a YTD foundation, the fund has declined 2.1% however has compounded at a stellar 8.5% price in market worth phrases (7.7% in NAV phrases) since its inception in 1994. On a 3, 5, and ten-year foundation, nonetheless, the fund has underperformed the benchmark, returning -3.4%, -1.6%, and three.0%, respectively. Distributions are paid out on a semi-annual foundation; up to now, the fund has distributed $1.30/share for 2022, although most of this has come from realizing capital beneficial properties. The revenue portion has been risky, with no payout since 2020. As this can be a fund with outsized publicity to high-growth tech and shopper names that favor reinvestments over distributions, the distribution is prone to stay low via the approaching years as nicely. Therefore, TDF is not an incredible match for revenue buyers.

Templeton

Path Cleared for a Shopper-Led Rebound

The important thing constructive from this month’s NPC meeting was the constructive commentary on the non-public sector – a reversal from the prior crackdowns over the past 12 months. The brand new Vice Premier and outgoing Nationwide Growth and Reform Fee (NDRC) head, He Lifeng, burdened the central authorities’s assist for the non-public sector in his speech, citing the worth of entrepreneurship as an engine of job creation and the significance of personal property rights. Additionally notable was the acknowledgment of ‘new industries’ like next-generation tech, electrical and autonomous autos, in addition to biotech, and their rising contribution to China’s GDP. Given the significance of employment and wealth creation to reigniting financial progress, the message signifies rising pragmatism from the federal government and bodes nicely for a tech/consumer-led rebound.

In the meantime, the newest China credit score information this month highlighted the rising traction that the PBoC’s financial easing is driving throughout the mainland financial system. With financial institution mortgage progress accelerating to >11% YoY and private-sector credit score progress additionally as much as ~9% YoY, the trail is obvious for pent-up demand to be unleashed after years of tight COVID-related restrictions. Intuitively, the sectors which have been most impacted ought to benefit from the greatest reopening enhance, and early information seems to assist this view. Retail gross sales progress has already reversed final 12 months’s declines however seemingly stays within the early innings at up low-single-digits % YoY within the preliminary months of 2023 (vs. a low-single-digit % YoY decline in December). Because the amassed extra financial savings by Chinese language households via the pandemic unwinds within the coming months, count on an extra acceleration within the consumption restoration; riskier property like property and monetary markets ought to profit from the incremental inflows.

Bloomberg

Mitigating Delisting Dangers by way of TDF

Investing via an actively managed fund like TDF comes with the next expense ratio (albeit on the decrease finish of comparable funds at ~1.4%), however buyers additionally get the good thing about extra flexibility – an more and more vital issue within the face of ever-escalating geopolitical tensions between China and the West. In a worst-case state of affairs, we may see de-listings of abroad inventory issuances (e.g., the US-listed ADRs) and even Chinese language equities being faraway from funding benchmarks, as we noticed with Russia final 12 months. Thus, TDF’s geographical flexibility to rotate out and in of share lessons throughout geographies is efficacious.

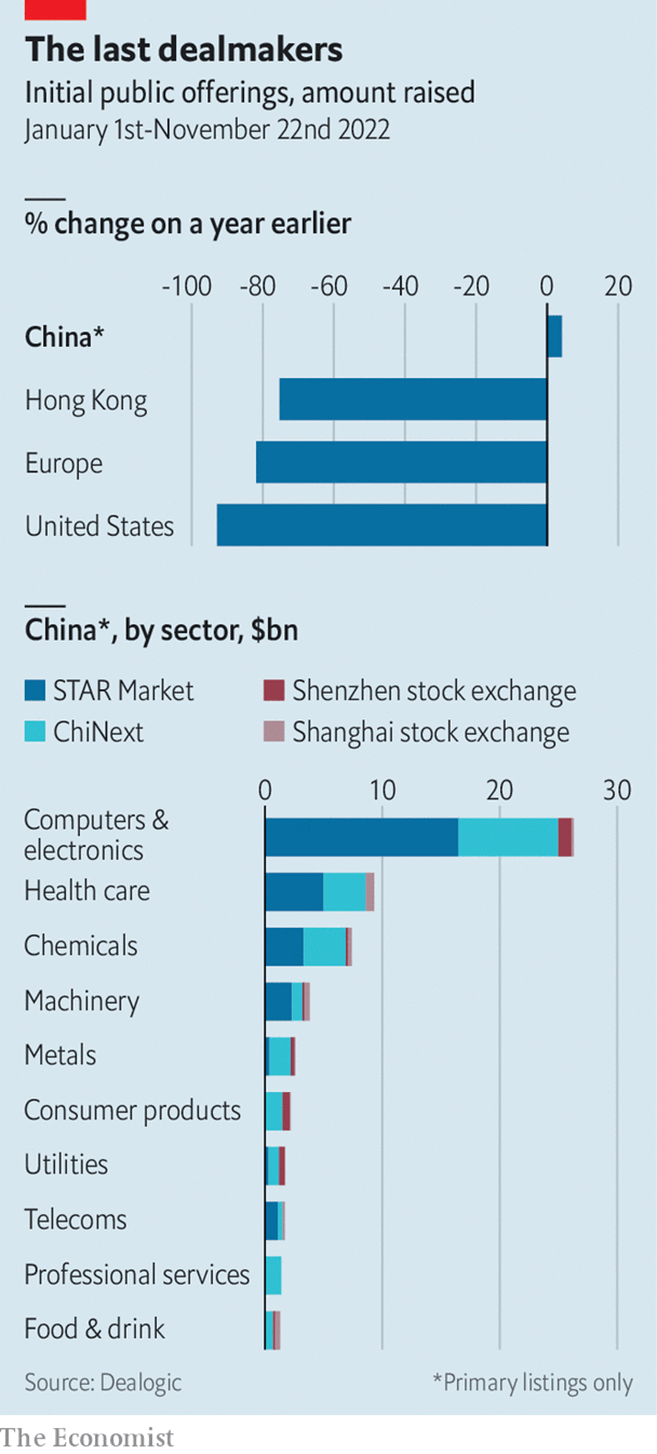

For now, the A-share market is the place to be – over the past weeks, the variety of A shares qualifying for the Northbound Inventory Join has increased significantly as Chinese language capital markets proceed to open up. This follows final 12 months’s rise in mainland equity issuances, in distinction to capital markets tightening up within the West amid the continuing financial tightening. As of November final 12 months, >$60bn had been raised on Chinese language exchanges, far outpacing issuances in New York and Hong Kong. The important thing sector that benefited was electronics and associated tech corporations that align with authorities insurance policies. If the current NPC was any indication, count on extra of the identical this 12 months as China reprioritizes financial progress and employment.

The Economist

An Actively Managed Choice to Trip the China Reopening Wave

With China nicely on observe for an accelerated GDP progress 12 months following the tip of its zero-COVID restrictions, the near-term tempo of home demand progress can be key to a sustained equities rebound. Alongside the continuing financial easing by the central financial institution, there stays ample pent-up demand but to be unleashed, given the huge family financial savings constructed up throughout the pandemic. As revenue progress additionally picks up post-reopening, count on a reallocation again into riskier property to assist a re-rating. In the meantime, exterior weak spot means future earnings progress revisions will seemingly be led by home consumption vs. exports, so enjoying the reopening theme by way of a consumer-focused fund like TDF is sensible. Whereas TDF’s lively administration comes with the next expense ratio (albeit on the decrease finish of comparable funds), it additionally permits for flexibility ought to any geopolitical headwinds come up, significantly with regard to abroad listings. With the NAV low cost now within the mid-teens %, TDF is price a glance right here.

pong6400

China seems to be poised to be the one main financial system to see an acceleration of GDP progress this 12 months amid a post-COVID restoration led by home demand. With cash provide progress additionally accelerating amid a rebound in key financial information factors (e.g., PMI and retail gross sales numbers), the near-term setup for Chinese language equities stays compelling. The unwinding of the huge family deposit build-up throughout the COVID-impacted years can be one other key tailwind all year long as family incomes recuperate and capital is reallocated into riskier property. To capitalize on a possible rebound, I’d favor an allocation to funds with increased home consumer-based publicity vs. externally derived revenue streams. Given its consumer-focused allocation, the Templeton Dragon Fund (NYSE:TDF) is a good choose inside the actively managed universe; the flexibleness to rotate its asset allocation (e.g., A-shares vs. US-listed ADRs) to mitigate geopolitical dangers is a bonus.

Fund Overview – Actively Managed, Shopper-Targeted Chinese language Publicity

The NYSE-listed Templeton Dragon Fund seeks to ship long-term capital appreciation by investing >45% of its property in Chinese language equities. The fund’s benchmark is the MSCI China All Shares Index, which tracks massive and mid-cap Chinese language equities throughout share lessons in Hong Kong, Shanghai, Shenzhen, and past. The ETF held $410m of web property on the time of writing and charged a 1.4% expense ratio (gross and web), inserting it on the decrease finish of comparable actively managed China obtainable to US buyers. Key information on the ETF is as per the graphic beneath:

Templeton

As mirrored within the chart beneath, the fund maintains an obese on the Chinese language shopper, with Retailing (14.0% vs. 11.1% benchmark) and Media & Leisure (13.2% vs. 11.6% benchmark) main the best way. Shopper Durables & Attire is the biggest obese by %pt at 8.0% in comparison with 2.3% for the benchmark, reflecting the fund’s leverage to a consumer-led rebound. Rounding out the top-five sectors are Capital Items (9.1%), Supplies (8.6%), and Prescription drugs, Biotechnology & Life Sciences (8.2%). In complete, the top-five sectors accounted for 53.0% of the overall portfolio.

Templeton

The fund’s largest single-stock holdings are Chinese language tech and leisure large Tencent Holdings (OTCPK:TCEHY) (8.9%), Chinese language e-commerce chief Alibaba Group (BABA) (5.9%), industrial banking chief China Retailers Financial institution (OTCPK:CIHKY) (4.9%), Chinese language sports activities gear firm ANTA Sports activities (OTCPK:ANPDY) (3.6%) and Chinese language buying platform Meituan (OTCPK:MPNGF) (2.9%). The portfolio consists of 67 holdings (vs. 789 for the benchmark index), with the highest 5 holdings accounting for ~26% of the general portfolio. Of observe, the fund is primarily made up of H/A shares, so buyers involved about regulatory dangers related to abroad listings (e.g., US-listed ADRs) might choose China publicity by way of TDF.

Templeton

On a YTD foundation, the fund has declined 2.1% however has compounded at a stellar 8.5% price in market worth phrases (7.7% in NAV phrases) since its inception in 1994. On a 3, 5, and ten-year foundation, nonetheless, the fund has underperformed the benchmark, returning -3.4%, -1.6%, and three.0%, respectively. Distributions are paid out on a semi-annual foundation; up to now, the fund has distributed $1.30/share for 2022, although most of this has come from realizing capital beneficial properties. The revenue portion has been risky, with no payout since 2020. As this can be a fund with outsized publicity to high-growth tech and shopper names that favor reinvestments over distributions, the distribution is prone to stay low via the approaching years as nicely. Therefore, TDF is not an incredible match for revenue buyers.

Templeton

Path Cleared for a Shopper-Led Rebound

The important thing constructive from this month’s NPC meeting was the constructive commentary on the non-public sector – a reversal from the prior crackdowns over the past 12 months. The brand new Vice Premier and outgoing Nationwide Growth and Reform Fee (NDRC) head, He Lifeng, burdened the central authorities’s assist for the non-public sector in his speech, citing the worth of entrepreneurship as an engine of job creation and the significance of personal property rights. Additionally notable was the acknowledgment of ‘new industries’ like next-generation tech, electrical and autonomous autos, in addition to biotech, and their rising contribution to China’s GDP. Given the significance of employment and wealth creation to reigniting financial progress, the message signifies rising pragmatism from the federal government and bodes nicely for a tech/consumer-led rebound.

In the meantime, the newest China credit score information this month highlighted the rising traction that the PBoC’s financial easing is driving throughout the mainland financial system. With financial institution mortgage progress accelerating to >11% YoY and private-sector credit score progress additionally as much as ~9% YoY, the trail is obvious for pent-up demand to be unleashed after years of tight COVID-related restrictions. Intuitively, the sectors which have been most impacted ought to benefit from the greatest reopening enhance, and early information seems to assist this view. Retail gross sales progress has already reversed final 12 months’s declines however seemingly stays within the early innings at up low-single-digits % YoY within the preliminary months of 2023 (vs. a low-single-digit % YoY decline in December). Because the amassed extra financial savings by Chinese language households via the pandemic unwinds within the coming months, count on an extra acceleration within the consumption restoration; riskier property like property and monetary markets ought to profit from the incremental inflows.

Bloomberg

Mitigating Delisting Dangers by way of TDF

Investing via an actively managed fund like TDF comes with the next expense ratio (albeit on the decrease finish of comparable funds at ~1.4%), however buyers additionally get the good thing about extra flexibility – an more and more vital issue within the face of ever-escalating geopolitical tensions between China and the West. In a worst-case state of affairs, we may see de-listings of abroad inventory issuances (e.g., the US-listed ADRs) and even Chinese language equities being faraway from funding benchmarks, as we noticed with Russia final 12 months. Thus, TDF’s geographical flexibility to rotate out and in of share lessons throughout geographies is efficacious.

For now, the A-share market is the place to be – over the past weeks, the variety of A shares qualifying for the Northbound Inventory Join has increased significantly as Chinese language capital markets proceed to open up. This follows final 12 months’s rise in mainland equity issuances, in distinction to capital markets tightening up within the West amid the continuing financial tightening. As of November final 12 months, >$60bn had been raised on Chinese language exchanges, far outpacing issuances in New York and Hong Kong. The important thing sector that benefited was electronics and associated tech corporations that align with authorities insurance policies. If the current NPC was any indication, count on extra of the identical this 12 months as China reprioritizes financial progress and employment.

The Economist

An Actively Managed Choice to Trip the China Reopening Wave

With China nicely on observe for an accelerated GDP progress 12 months following the tip of its zero-COVID restrictions, the near-term tempo of home demand progress can be key to a sustained equities rebound. Alongside the continuing financial easing by the central financial institution, there stays ample pent-up demand but to be unleashed, given the huge family financial savings constructed up throughout the pandemic. As revenue progress additionally picks up post-reopening, count on a reallocation again into riskier property to assist a re-rating. In the meantime, exterior weak spot means future earnings progress revisions will seemingly be led by home consumption vs. exports, so enjoying the reopening theme by way of a consumer-focused fund like TDF is sensible. Whereas TDF’s lively administration comes with the next expense ratio (albeit on the decrease finish of comparable funds), it additionally permits for flexibility ought to any geopolitical headwinds come up, significantly with regard to abroad listings. With the NAV low cost now within the mid-teens %, TDF is price a glance right here.

{kind=link}