francescoch/iStock by way of Getty Photographs

It was the most effective of instances, it was the worst of instances. It was the age of knowledge, it was the age of foolishness. It was the epoch of perception, it was the epoch of incredulity. It was the season of sunshine, it was the season of darkness. It was the spring of hope, it was the winter of despair.

–Charles Dickens, A Story of Two Cities

I will be trustworthy with you: I could not get by way of Dickens’ well-known novel, A Story of Two Cities, in highschool. Maybe it could have been gripping to an 1860 Londoner, however to a mid-2000s American teenager, it could not have felt extra tedious and inscrutable.

Maybe the best contribution to the world made by Mr. Dickens’, together with Shakespeare and others, was to gas the rise of SparkNotes and different chapter summaries of excessive literature.

The actual “story of two cities” is the disparity between how a lot highschool English academics appear to like Dickens versus how a lot youngsters hate it.

Now, with that off my chest, I have to admit that Dickens’ opening line is a strong and poetic expression of the nice disparities that exist on the earth. It feels true of many issues: two extremes, aspect by aspect, veiled by the tyranny of averages.

That, I might argue, is strictly the state of affairs we discover within the inventory market in the present day.

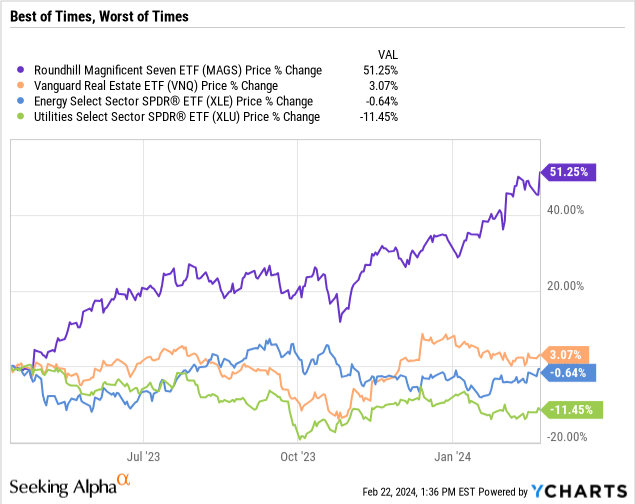

Evaluate, for instance, the efficiency of the Magnificent 7 (MAGS) to that of out-of-favor sectors like actual property (VNQ), power (XLE), and utilities (XLU) over the previous yr:

It has been stunning to see the diploma to which Large Tech more and more luxuriates in oceans of money whereas historically defensive sectors battle for measly scraps.

As I acknowledged in “The Magnificent 7 Dividend Stocks For 2024,” the Magnificent 7 mega-cap firms actually are magnificent.

This was demonstrated most lately in Nvidia’s (NVDA) magnificent This fall 2023 earnings launch, wherein CEO Jensen Huang highlighted generative AI as a burgeoning expertise being adopted by every kind of industries (auto, healthcare, monetary companies, robotics, and so forth.) to streamline operations and increase development.

Generative AI and huge language fashions are clearly extra than simply hype. They’re producing huge revenue development for business leaders like NVDA. NVDA’s EPS practically quadrupled from 2023 to 2024.

Whereas such wild success inevitably attracts competitors, and the biggest constituents of inventory indices hardly ever stay the identical from decade to decade, it doesn’t look inevitable that the Magazine 7 will quickly be lower all the way down to dimension. Fairly the other. Their reign, actually for the superstars in generative AI like NVDA, doesn’t seem like ending anytime quickly.

In what follows, I am going to focus on some charts displaying the intense disparity current within the inventory market in the present day. Then I am going to check out how my “Magnificent 7 Dividend Shares” from the above-linked article are performing in opposition to the Magazine 7 year-to-date. (Preview: It ain’t fairly.)

The Spring of Hope and Winter of Despair

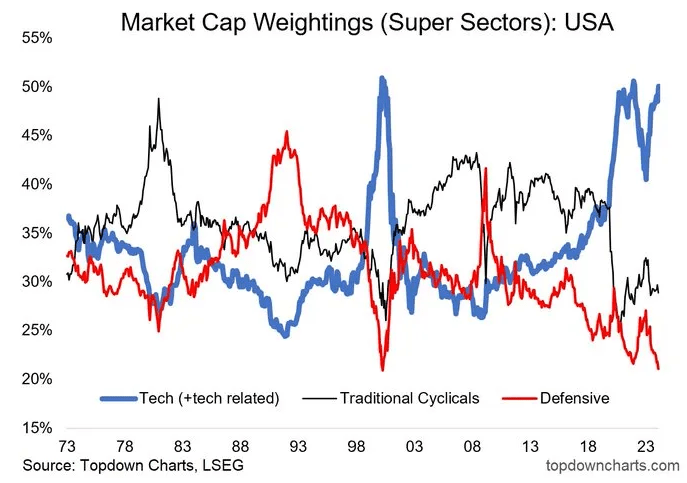

The expertise sector has not made up this a lot of the general inventory market (by market cap weighting) since… you guessed it… the dot-com bubble of 2000.

Topdown Charts

On the similar time, defensive sectors like utilities, shopper staples, and healthcare haven’t been such a small portion of the broad market for the reason that dot-com bubble.

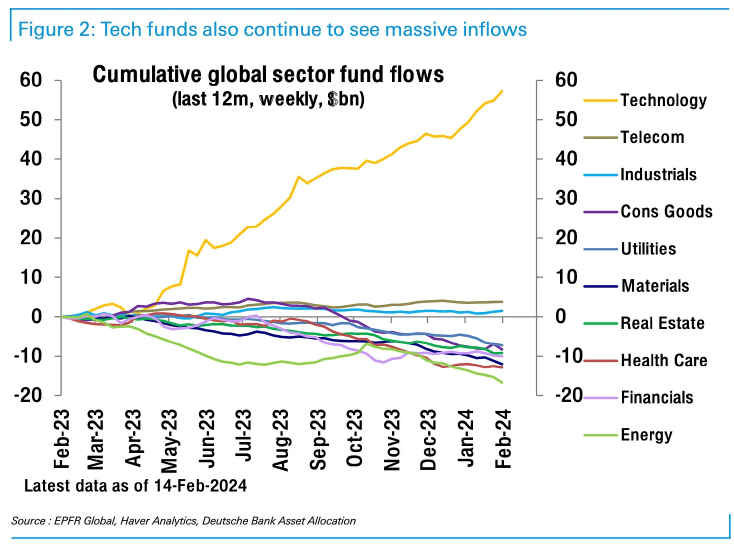

During the last yr, the huge (and I imply huge) majority of inventory sector fund inflows have gone into tech.

Deutsche Financial institution

Communications (VOX) has loved some inflows primarily due to names like Meta Platforms (META), Alphabet (GOOGL), and Netflix (NFLX) — all up massively over the past yr. Industrials (VIS) have likewise held their floor.

All different sectors have seen web outflows over the previous yr.

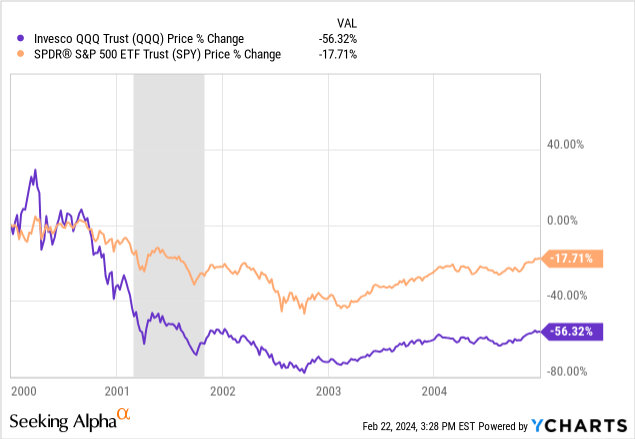

We’ve not seen such famously spectacular efficiency from an iconic group of shares for the reason that “Nifty Fifty” of the late Nineteen Sixties and early Seventies. Again then, the prevailing angle was that the Nifty Fifty had been actually all you wanted to personal as an investor. That angle appears to be current in the present day as properly.

Deutsche Financial institution

The Magazine 7 presently account for about 33% (1/third!) of the S&P 500’s whole market cap.

You’ll be able to see that on the peak of the 2022 selloff, Berkshire Hathaway (BRK.A, BRK.B) ascended into the highest 5 largest firms by market cap. Some inexperienced shoots of worth started to appear. However when tech rallied in 2023, the reign of development over worth promptly resumed.

The controversy between worth and development buyers is whether or not in the present day’s state of affairs “rhymes” with that of the dot-com bubble or not.

The worth camp says sure, in the present day’s generative AI hype is just like the Web hype of the late Nineteen Nineties. And, they are saying, whereas the tech sector sucked up all of the oxygen within the room again then, just about each sector benefited from the adoption of the Web. The identical will maintain true with generative AI. Buyers are throwing their cash at a handful of tech firms on the forefront of the AI hype, however every kind of firms and industries will find yourself benefiting from the industrial adoption of AI. The Magazine 7 will ultimately undergo a interval of underperformance identical to the Nasdaq index (QQQ) did after the dot-com bubble burst.

However, the expansion camp says no, in the present day’s state of affairs may be very totally different than the Web hype cycle of the late Nineteen Nineties.

Not like in the present day’s Nasdaq index P/E ratio of about 27x, the index sported a nosebleed P/E ratio of about 175x at its peak in March 2000.

At this time, in contrast to then, mega-cap firms are quickly turning hype into revenue development, which ends up in the Magazine 7 having a decrease PEG ratio than the entire S&P 500 index (SPY) or the MidCap S&P 400 index (MDY).

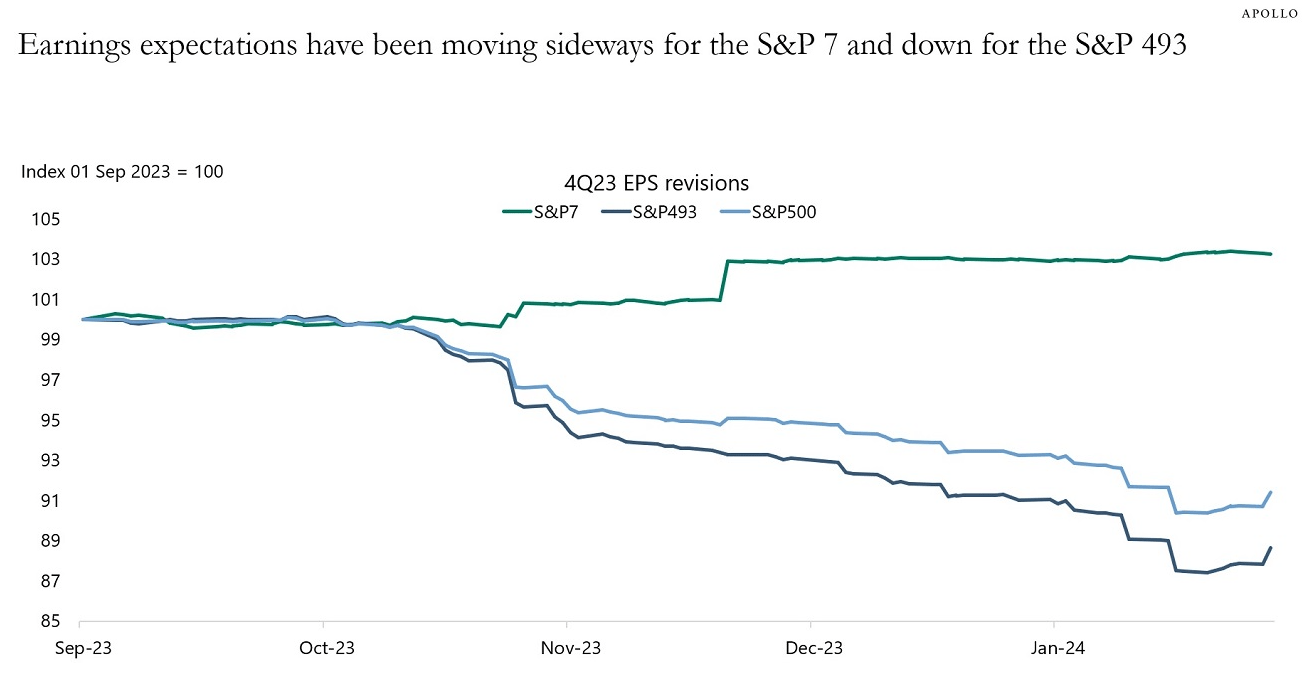

Factset

The truth is, whereas the chart beneath is a bit dated now, it does present the unbelievable divergence between earnings estimates trending upward for the Magazine 7 and downward for the remainder of the SPY.

The Every day Spark

It’s the better of instances within the techy AI world, and it’s the worst of instances in most different elements of the inventory market, particularly cyclical industries and curiosity rate-sensitive firms.

Because the starting of 2022, mentions of weak demand (and variations thereof) have soared to ranges reserved just for recessionary durations.

Financial institution of America International Analysis

The Fed’s “increased for longer” regime has been punishing for enterprise fashions that rely closely on the usage of debt, most notably industrial actual property.

Within the realm of REITs, refinancing debt maturities is pressuring earnings similtaneously tenant demand is receding and a wave of latest provide is coming on-line.

Utilities are shouldering the burden of upper curiosity prices from each debt refinancing and new issuance to fund aggressive capability growth.

Shopper staples are reaching the top of the numerous worth hikes that buyers can or will bear whereas concurrently combating off low-margin, private-label competitors and attempting to deleverage.

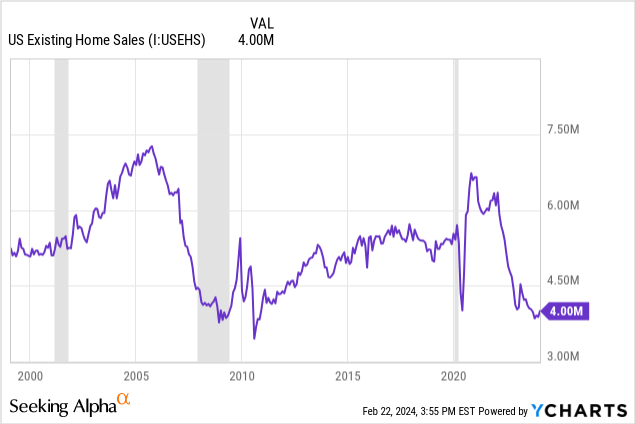

And the housing market, together with the various industries it helps, is languishing from the bottom dwelling gross sales quantity for the reason that Nice Monetary Disaster of 2008-2009.

In different phrases, a fantastic many industries and sectors face a scarcity of money and are seemingly “combating for scraps.”

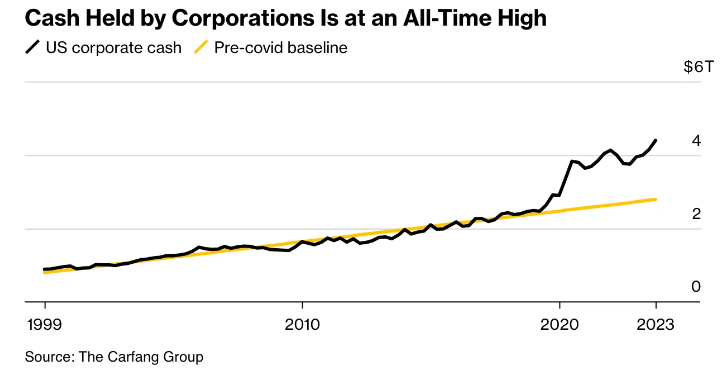

On the similar time, weak point throughout a broad swathe of the economic system and enterprise world is masked by the tyranny of averages. For instance, one may level to this chart for instance the truth that company America is doing higher than ever and has loads of money within the financial institution:

The Carfang Group

However the majority of this money is held by a comparatively small variety of firms, primarily in tech, insurance coverage, and funding banking.

The Magazine 7 firms alone account for over 10% of whole US company money holdings.

This money is now producing curiosity at over 5% yields, which performs a task within the Magazine 7’s super outperformance in the course of the Fed’s price mountaineering cycle.

Take into account, for instance, that Alphabet’s ~$111 billion in money could possibly be producing about $5.5 billion in annualized curiosity. That represents about 7.5% of the corporate’s trailing twelve month web revenue!

“Larger for longer” tremendously advantages the Magazine 7 and tremendously hurts many different elements of the economic system.

A Humble Dividend Investor’s Perspective

I’m not an investor within the Magazine 7, apart from some small publicity to 3 of them by way of the WisdomTree US High quality Dividend Progress ETF (DGRW).

I’m not a Magazine 7 denier, both. I acknowledge that they’re, by and huge, unbelievable firms with robust development prospects.

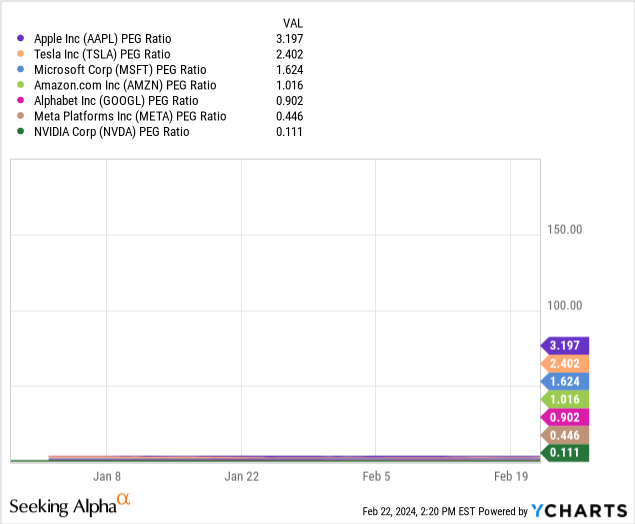

However some are higher valued relative to their development prospects than others. For instance, in the event you escape the Magazine 7’s price-to-earnings development (PEG ratio) by particular person firm, you may discover vast variation between Apple’s (AAPL) ~3.2x and NVDA’s 0.1x.

If the PEG ratio is to be trusted, then maybe AAPL’s inventory is overhyped whereas NVDA’s is (brace your self) underhyped, although NVDA has vastly outperformed AAPL over the past yr.

All I’m saying is that maybe some members of the Magazine 7 are extra deserving of their wealthy valuations than others.

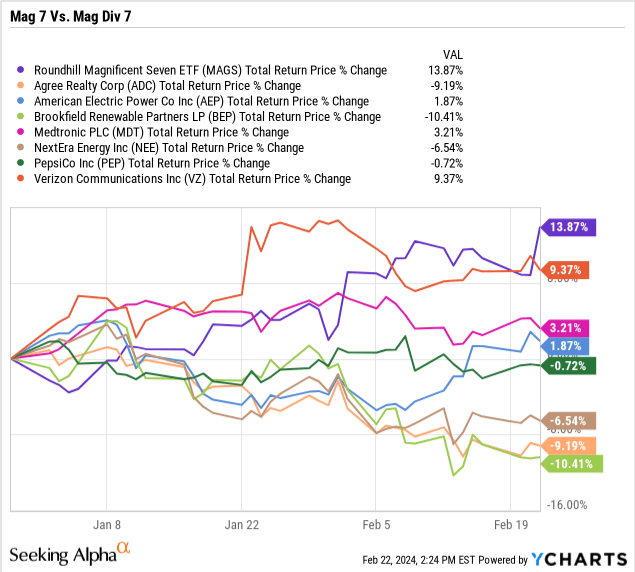

Now, what about my (thus far, ill-fated) guess on the “Magnificent 7 Dividend Shares” to beat the Magazine 7 in 2024?

I will not lie. It hasn’t turned out that properly thus far.

Verizon (VZ), of all shares, briefly outperformed the Magazine 7 in January, solely to be overtaken in February.

However I proceed to imagine that when the market can see the whites within the eyes of Fed price cuts, beleaguered sectors like REITs, utilities, and different dividend shares ought to take pleasure in their time within the solar once more.

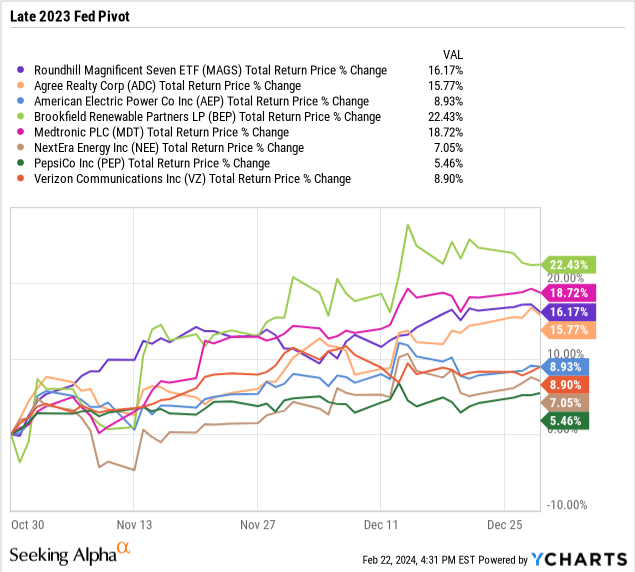

Should you have a look at the two-month interval on the finish of 2023 (I do know it isn’t a big pattern dimension), dividend shares’ efficiency was much more respectable in opposition to the Magazine 7.

The Magazine 7 nonetheless beat most of my Magnificent 7 Dividend Shares, however the debt-laden Brookfield Renewable (BEP, BEPC) and medical gadget maker Medtronic (MDT) each outperformed, and high-quality web lease REIT Agree Realty (ADC), which the market treats like a bond proxy, was proper on the Magazine 7’s heels.

Does this group of dividend shares have any probability at overcoming their early-year deficit and staging a comeback to outperform the Magazine 7 for the steadiness of the yr?

I believe that can closely depend upon what the Fed says and does over the course of the yr.

For now, we dividend buyers are nonetheless principally dwelling within the “worst of instances.”

{kind=link}